Mr. Geheran said, “I haven’t seen [structural separation] work anywhere globally, to sustainable effect,” to which Calgary-Nose Hill MP Michelle Rempel Garner replied, “It’s in the UK, right?”

Mr. Geheran responded, “But if you look at the UK, they are wholesale moaning about the quality of their infrastructure, their lack of fibre coverage. across what is a very small geography. I know. I originated from there. And quite frankly, the Canadian networks are far superior in coverage and quality and performance through COVID has demonstrated that.”

Recently, that committee adopted a report, “Affordability and Accessibility of Telecommunications Services in Canada: Encouraging Competition to (Finally) Bridge the Digital Divide” [pdf, 3.4MB], that had been released by the Committee during the previous session of Parliament. I found it interesting that the Parliamentary Committee report did not recommend studying structural separation, despite a specific call for such a strong competitive safeguard from at least one of the witnesses. However, in its more recent report examining the Rogers – Shaw transaction [pdf, 3.1MB], that same committee suggested studying the matter further:

Recommendation 1: That the Government of Canada launch nationwide consultations to examine the implementation of structural separation in the telecommunications sector between businesses that build infrastructure and those that provide services in order to ensure a level playing field that fosters network development in both cities and rural areas.

As it turns out, the CRTC has already held nationwide consultations that examined proposals such as structural separation. In 2015, as part of its review of wholesale wireline services, the CRTC examined a CNOC proposal to implement an “Equivalence of Inputs” regime, a very basic form of structural separation, “such that any wholesale service offered by an incumbent carrier to a competitor be provided at the same price, quality, terms and conditions, and timescale, using the same systems and processes that incumbent carriers’ use in their wholesale operations to supply their own retail operations”. The Commission rejected the proposal, saying it “would represent an overly intrusive regulatory measure, which would neither be efficient nor proportionate to its purpose“.

As a regulatory measure, structural separation has rarely been used in wireline broadband markets, and only where there is a single dominant network operator. To my knowledge, it has never been used in the wireless industry.

Unlike some foreign markets, in Canada there is no single network with a dominant presence. For example, in the UK, BT agreed to separate its wholesale and retail operations into separate business units after the regulator concluded that it had a natural monopoly over phone and broadband infrastructure in the UK. In other words, if you wanted phone or broadband services, you had to use the BT network.

In contrast, Canada’s wireline and wireless broadband networks are provided by multiple national and regional wireline and wireless service providers. As discussed recently in “Truthiness and Canada’s Telecom Industry”, Canada has the least concentrated broadband market in the G7 plus Australia. Upon which network would separation be imposed?

Just as proponents of mandated wholesale MVNO access have been pushing for a wholesale model that has been tried and largely abandoned elsewhere, proponents of structural separation are pushing another form of regulatory intervention that has fallen out of favour.

As described in Federal Communications Law Journal [pdf, 2.9MB], “Concerns about the potential for such disruptions [in economic efficiencies]–combined with recognition that the more extreme forms of separation potentially are irreversible-have led most regulators to back away from mandatory separation, or to view it as a “last resort,” to be used only in cases of extreme and otherwise irremediable discrimination.” The authors indicate that separation “may discourage the introduction of new networks, thereby reducing economic welfare and harming consumers.” Further, “the available evidence fails to support the proposition that mandatory separation improves market performance, but this evidence does suggest that such a policy leads to reduced levels of innovation and investment.”

Reduced levels of innovation and investment would fail to deliver the Parliamentary Committee’s stated goal of “[fostering] network development in both cities and rural areas”.

Canada needs regulatory policies that create incentives for more investment and innovation, not less.

As some will recall, prior to becoming a talk show host, Stephen Colbert starred as a right-wing pundit on a satirical news show entitled The Colbert Report. Colbert, the pundit, was billed as America’s most fearless purveyor of “truthiness”. What is truthiness? It’s “the belief or assertion that a particular statement is true based on the intuition or perceptions without regard to evidence, logic, intellectual examination, or facts”.

Giving elected officials the chance to ask questions of regulators is an important part of our democratic process. It can be very informative when used wisely. Unfortunately, the opportunity is wasted if Committee members are unprepared or do not have a solid understanding of the industries they are overseeing.

There was a lot of truthiness on display at INDU as Committee members repeated inaccuracies about wholesale internet access rates, the state of competition in the wireless industry, the reasons for the lack of foreign entry, and the role of MVNOs in the wireless market. Some of these topics were discussed in my post last year (“Mythbusting Canadian Telecom”), but these misunderstandings refuse to go away and deserve revisiting.

Myth #1: The CRTC raised wholesale internet access rates

Few regulatory files have been as misunderstood as the setting of wholesale rates for internet service providers (ISPs) dependent on using facilities of carriers that have invested billions in building Canada’s digital infrastructure. These reseller ISPs operate using connections built by wireline carriers, paying wholesale rates that are set by the CRTC.

For as long as I have been around, these rates have been in dispute. Indeed, the interconnection architectures have been subjects of multiple regulatory battles as independent service providers seek alternate ways to arbitrage the connections provided by the facilities-based service providers [see, for example, the CRTC’s wholesale services framework set in July 2015].

The latest rates dispute actually began in May 2015, when the CRTC began a “Review of costing inputs and application process for wholesale high-speed access services.” In early 2016, the CRTC resolved that consultation and made a determination on processes to set the wholesale rates. In October 2016, the CRTC established substantially lower wholesale rates that it designated as “interim” while it undertook a more extensive review. These interim rates reduced the transport component by up to 89%, and the access component rates by up to 39%. Notably, at the time, CNOC issued a statement saying “The CRTC’s actions will immediately benefit both Canadian consumers and businesses and we are hopeful that the final outcome of this matter will have the same result.”

In 2019, the CRTC issued its “final” determination, setting rates that lowered the rates even more, rates that the Commission later acknowledged were based on mistakes. Those 2019 wholesale rates were never given effect; the 2019 decision was immediately made the subject of multiple channels of appeal and the rates were stayed. In May 2021, the CRTC finalized the rates and issued a wholesale broadband service background paper describing the process.

As the CRTC Chair told INDU, “When we analyzed the evidence, we found errors and could no longer justify the associated rates. Ultimately, we chose to reaffirm and make final the interim rates that we set in 2016, with some adjustments.”

Most importantly, as INDU was told, “the 2019 rates were never in effect in the marketplace.”

The CRTC did not raise wholesale internet access rates. It lowered them.

Myth #2: Canada has a lack of competition compared to other countries

Many have heard it said that the Canadian wireless market is less competitive and more concentrated than in other countries. But how many making such statements have bothered to look at the state of competition in other markets?

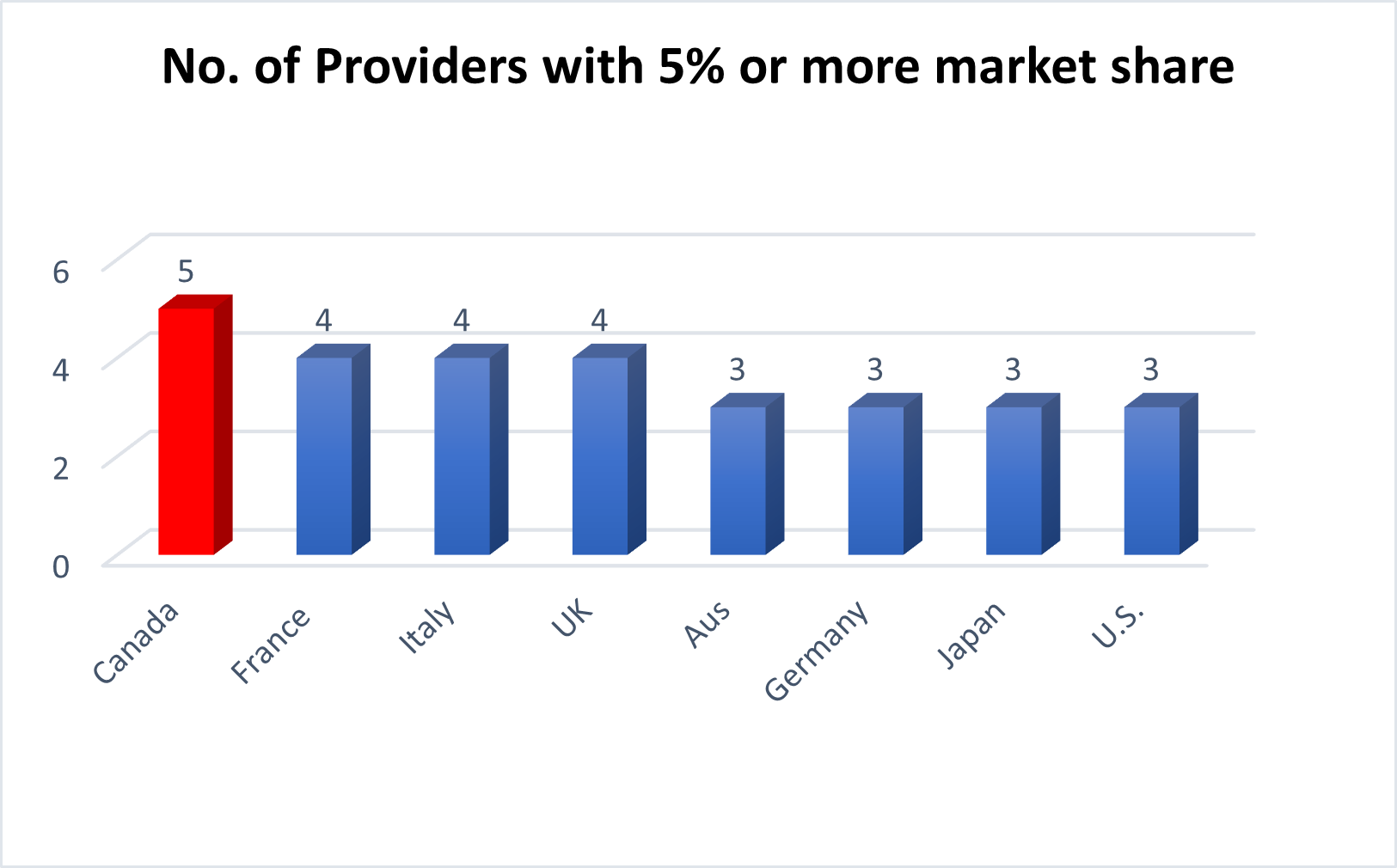

Figure 1

I decided to do just that.

[Note: The data in Figures 1 through 4 is from Telegeography (September 2021). The source data for Figure 5 is The Economist Intelligence Unit – The Inclusive Internet Index – 2021]

One way to look at competition is by the number of mobile wireless carriers in each market. If you listen to some commentators, you might assume that Canada has fewer carriers than most other countries.

In fact, the opposite is true.

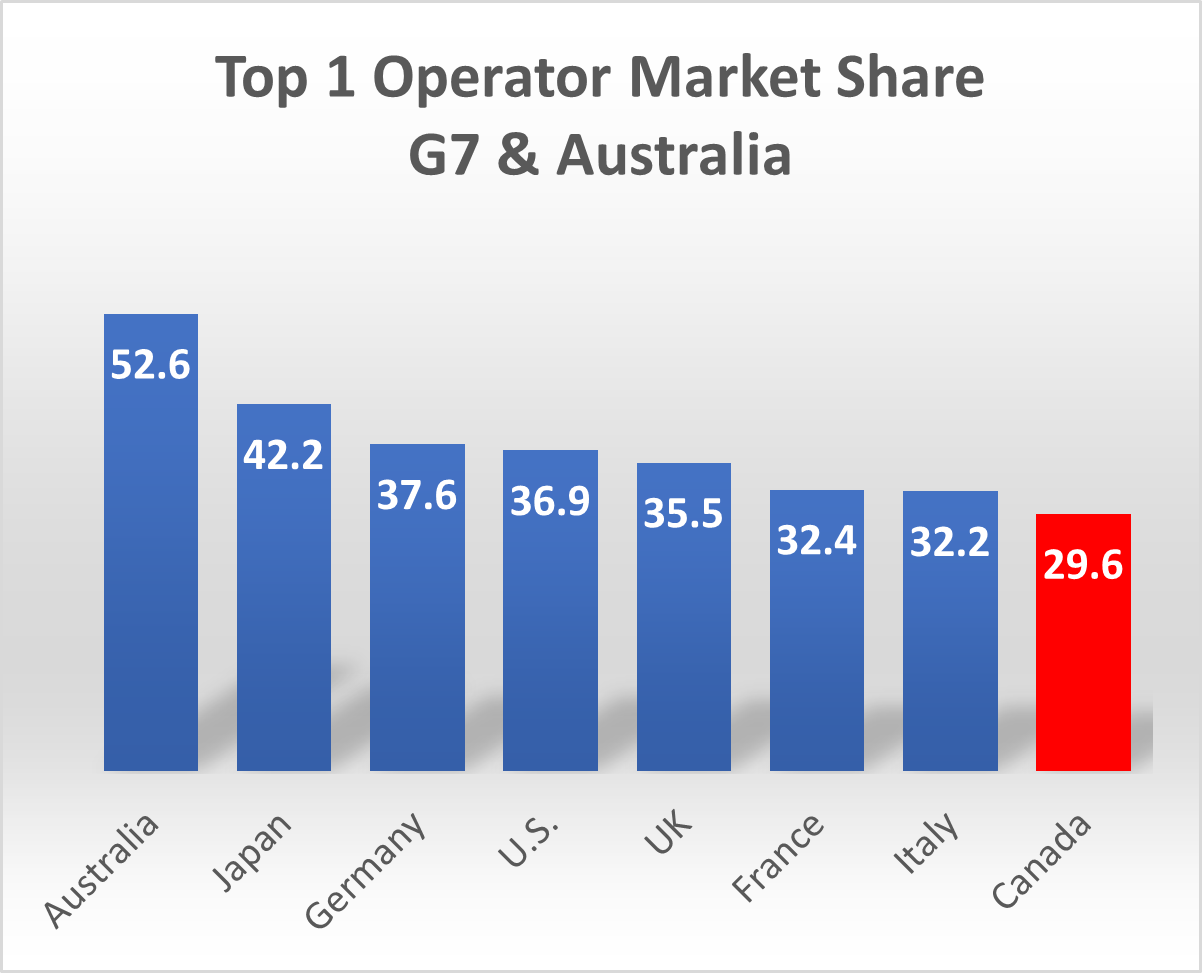

Figure 2

As shown in Figure 1, Canada has more mobile service providers with a 5% market share than any other country in the G7 plus Australia.

Some may respond by saying that despite having five carriers that surpass the 5% threshold, Canada’s three national carriers dominate the market.

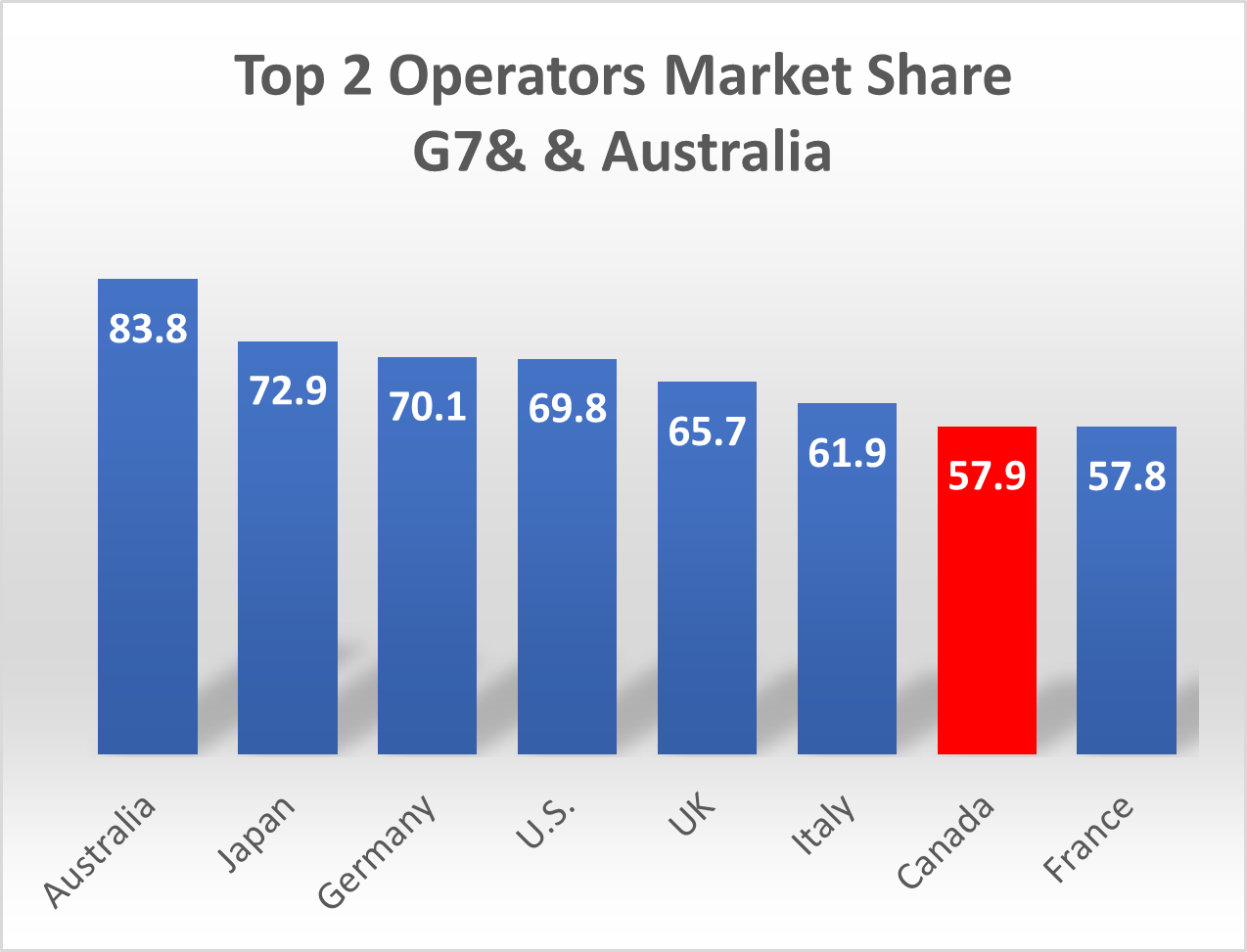

Figure 3

Sure, the national carriers are bigger than the regional providers, but does that make Canada an outlier compared to its peers?

The facts show otherwise.

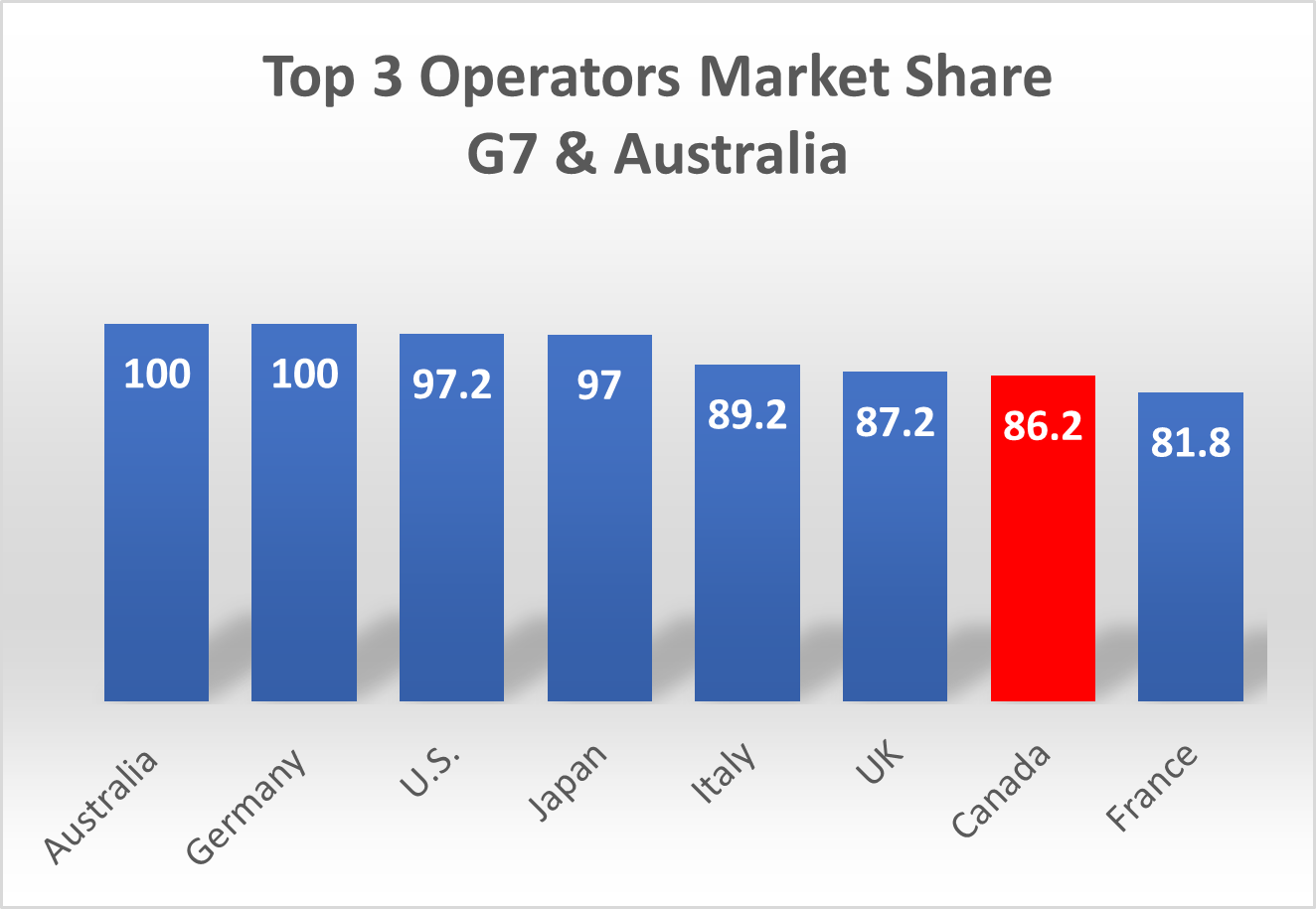

Figures 2, 3 and 4 illustrate that Canada’s wireless market is less concentrated than peer countries (other than France) when you look at the market share of the leading carrier, the share of the top two carriers, and the top three carriers.

Figure 4

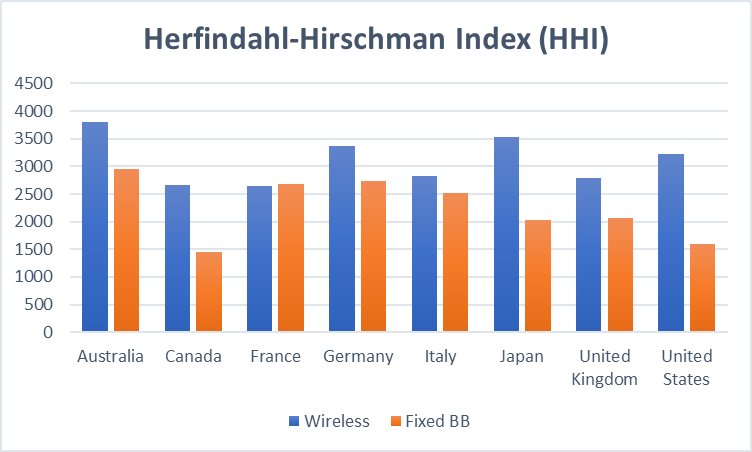

Another commonly accepted measure of market concentration is the Herfindahl-Hirschman Index (HHI). HHI is calculated by squaring the market share of each competing firm and then summing the result.

An HHI of 10,000 would indicate one company in a market with 100% market share, while a market of thousands of firms, each with less than 1% market share would have an HHI of close to zero. In other words, the lower the HHI, the less concentrated a market is.

Figure 5As Figure 5 illustrates, of the G7 countries plus Australia, Canada has the lowest HHI for fixed broadband markets and is in a virtual tie with France for lowest wireless market HHI.

Despite these facts, critics of Canada’s wireless industry continue to argue that a lack of competition is the cause of whatever aspect of the market they are rallying against.

Since it isn’t the competitive intensity, perhaps more attention should be paid to other factors that distinguish Canada from other countries.

For example, readers of this page know that I have frequently discussed the high quality and expansive coverage of Canada’s digital infrastructure, despite substantially higher costs associated with spectrum and building networks to serve Canada’s widely-dispersed and smaller population.

Myth #3: More MVNOs would reduce prices in Canada

At INDU, one MP suggested that the CRTC said “no” to Mobile Virtual Network Operators (MVNOs).

No, the CRTC did no such thing.

The Commission refused to mandate MVNOs, but that is the same as virtually every regulatory body around the world. And similar to most jurisdictions, MVNOs are indeed permitted in Canada.

And MVNOs actually exist in the Canadian market. But, implicit in the MP’s questioning was the idea that having more MVNOs would result in lower consumer prices. It’s an appealing argument, until you look at the facts and understand that the objective of MVNOs is not to lower prices, it is to make a profit.

Outside of China, the countries with the largest MVNO market are the US, Germany, and Japan. It is estimated that Japan has about 170 MNVOs. If there were a relationship between the number of MVNOs and lower prices, one would assume that these three countries would also have the lowest wireless prices. They do not. As shown by ISED’s most recent international price comparison report, wireless prices in these countries are similar to, and in some cases higher than, prices in Canada.

So why do these countries have so many MVNOs?

Mobile carriers in these countries decided that part of their business strategy would be to use resellers and other brands to acquire customers for their network services. In some cases, they use a sub-brand that they own; in other cases, they enter into a commercial arrangement with an independent brand. For the independent brand, the motivation is not to lower prices; like all businesses, their objective is to make a profit. Some were successful by targeting specific demographics or brand-aware groups, while many were unsuccessful and have gone out of business. But the bottom line remains: the number of MVNOs does not correlate to lower prices.

Myth #4: Foreign companies are not allowed to offer wireless services in Canada

I continue to be surprised at the persistence of this myth. But even more surprising was to hear a Conservative MP raise the issue at INDU, when almost ten years ago the Conservative-led government removed nearly all restrictions on foreign companies operating in the Canadian wireless market. The only remaining restriction is a foreign-owned company cannot gain entry by acquiring any of the three national carriers.

What is stopping them from launching a competing wireless business in Canada? I can only speculate, but I think it is reasonable to assume that they have looked at the amount of investment required to acquire spectrum and build out a network, the relatively small population of Canada, and, as discussed in Myth 1 above, the number of carriers already in the market, and concluded the business case simply does not work.

It is economics, not regulations, that drives their decision-making.

Why do I continue to address these myths?

I try to tackle these myths for the same reason I write this blog.

You cannot properly oversee a market that you do not understand. Canada and Canadians will not benefit from policies based upon the “truthiness” of feelings and perceptions.

Balancing the policy objectives of quality, network coverage, and affordability requires a deep understanding of the Canadian telecom market, how it compares to other countries, as well as looking at the positive and negative impacts of policy decisions made in other countries to try to avoid unintended consequences.

We can, and must, do better to ensure that the digital networks that helped maintain economic and social activity during the COVID-19 pandemic can propel Canada into a future of economic and social prosperity.

Canada’s future depends on continued investment in connectivity.

India has among the world’s lowest prices for mobile services. But India is learning that there is a cost to winning the race to the bottom.

Last week, Reuters reported that India’s federal cabinet approved a relief package for its telecoms sector, including a four-year moratorium on spectrum fees.

India’s telecoms sector ran into trouble in late 2016 with the entry of billionaire Mukesh Ambani’s Reliance Jio, sparking a price war that has forced some rivals out of the market and turned profits into losses.

Despite relief going forward, Indian carriers have billions of dollars in outstanding adjusted gross revenue payments owed to the government. Vodafone Idea owes roughly $7 billion in telecoms dues, according to Reuters’ examination of regulatory filings. Bharti Airtel owes the government $3.5 billion.

Price wars have produced great deals for consumers in the short term but service providers have been left unable to invest. A recent story in India Today says “India ranks 122nd globally in terms of mobile network speeds” according to data from Ookla, the company behind Speedtest.net.

Two years ago, I looked at a similar situation in Israel when I wrote “Low prices, at a high cost”. Following aggressive government intervention, prices in Israel fell, but so did the quality of the networks. “The massive reductions to revenues caused major reductions in capital expenditures, network roll-out and expansion, market capitalizations of the participants and even the number of employees.” As I said at the time, “The short term consumer benefits from policies driving low mobile prices may lead to higher and broader economic costs in the long run.”

A colleague of mine likes to say that a healthy telecom sector is one that generates sustainable competition, competition that is not just competing on price but also fostering investment in digital infrastructure to provide consumers with increasing quality of services.

As we have discussed so often before, it is a matter of balance. Two weeks ago, I wrote “there is a difference between “affordable prices” and “rock-bottom prices”.” There is a need to be able to cover the costs associated with expanding coverage and investment in advanced technologies.

India is another example of what happens when regulators and policy makers ignore the delicate balance between the competing objectives for: universal access; investment in high quality telecommunications services; and, at affordable prices.

Over the past two days, Rosh Hashana services have given me an opportunity to reflect on a variety of issues and, as might be expected, my mind turned to telecommunications.

Conservative leader Erin O’Toole released a policy statement on telecom on Tuesday, the first day of Rosh Hashana, saying

Canada’s Conservatives will let companies from Europe or the United States come to Canada and compete for your business. That will mean more choice and lower prices. Only Canada’s Conservatives have a plan to make cell phone and internet service more affordable for you.

Due to the holiday, I regret that it has taken a couple days to respond.

The Conservative backgrounder [pdf, 245KB] appears to be relying on Section 16(3) of the Telecom Act for its statement, “Currently, foreign ownership of a Canadian telecommunications company is limited to up to 20 per cent of a company’s voting shares and no more than 33.3 per cent of the voting shares of a holding company, and an effective total limit of 46.7 per cent as long as the foreign entity does not have control.”

Apparently, they read that section of the Act without reading S.16(2)(c) and S.16(6) which effectively combine to allow any company other than Rogers, Bell or TELUS to be foreign owned. So it simply isn’t true that “Canada currently bans foreign companies from competing here”, as Conservative leader Erin O’Toole said during the press conference.

The Conservative backgrounder starts off saying “A Conservative government will begin the process of allowing international telecommunications companies to provide services to Canadian customers, provided that the same treatment is reciprocated for Canadian companies in that company’s country.” A reciprocity test does not currently appear in the Telecom Act, so such a restriction would actually serve to limit the number of foreign competitors, not increase the pool.

Companies from Europe and the United States (and, for that matter, from the rest of the world) have been allowed into Canada for nearly a decade.

With new-entrant set-aside rules, these foreign competitors even had the opportunity to pick up spectrum at a substantial discount.

I have to ask, “Where are they?”

If consumer prices are really that much higher than costs, wouldn’t that have created even more of an incentive for others to enter the market?

It is good to see the Conservative platform examining the cost of spectrum, which has been identified as a significant contributor to higher carrier costs. Canadian spectrum costs have been called a hidden tax, contributing an extra 12% to our wireless bills. It appears to be a recognition that spectrum policy needs to be reviewed. It remains unclear how a promise like “A Conservative government will make investments in rural broadband and lowering prices a necessary criteria of winning spectrum auctions” would be significantly different from the current government’s tension balancing price, coverage and quality.

In the welcome letter to CRTC Chair Ian Scott four years ago, the Ministers wrote “All Canadians and Canadian businesses deserve high quality telecommunications services at affordable prices.”

They do. As I have noted many times, there is a difference between “affordable prices” and “rock-bottom prices”. And there are costs associated with expanded coverage and advanced technologies. Mr. O’Toole said at Tuesday’s media event “Canada’s Conservative will always put the interests of Canadian consumers first.”

No clear strategy. No clear objectives. No scorecard for measuring progress.

What are we trying to accomplish? How do we measure success? As I have said many times [here and here], I would like to see us start with clear objectives: “Set clear objectives. Align activities with the achievement of those objectives. Stop doing things that are contrary to the objectives.”

How do we celebrate success in digital policy, if we aren’t clear about what we are trying to do?

How do we move forward?

After the heat of the election battle has cooled down, we’ll want to watch for a clear strategy, recognizing the balance and inter-relationships between competing objectives for universal access to high quality telecommunications services at affordable prices.

It’s one thing to look at how we got to where we are; it’s something quite different to agree on where we want to go from here.

Only then can we figure out the best way to get there.

Price isn’t the only factor driving many consumer purchasing decisions, and telecom services are no different.

We know that quality and coverage are important factors as well. People are willing to pay more for faster speeds, greater reliability, and a host of other factors [see “Competition brings out the best”]. That isn’t to say price isn’t important. All else being equal, who doesn’t want to save money?

The thing is, all else is rarely equal.

Whether shopping for shoes, groceries, cars, clothes, telecom services or whatever, quite frequently, all else isn’t equal. As consumers, often there are other factors at play.

We might deal with the same car dealer years after our last purchase, or stick with the same brand of car. We find stores that we like – for a variety of reasons – and continue to deal with them, even if the price isn’t always the lowest. Maybe we have found the store employees are friendlier; or, the grocery store’s produce is fresher; or, the meat seems better.

The lowest price isn’t always the deciding factor.

We often speak of the regulatory and policy tension in balancing quality, coverage and price for telecommunications services [see, for example “Value, affordability and investment”].

It has become popular to use the term “affordability” to refer to the service offerings of the wholesale-based service provider community. That is misleading and wrong. Doing so is hijacking the term “affordability”.

The marginally lower priced offerings from wholesale-based service providers simply don’t offer such affordable options for those most vulnerable Canadian households. Indeed, it is doubtful the reseller community could compete with these truly affordable services, even if the CRTC’s flawed 2019 wholesale internet rates decision is restored.

It is disappointing to see a singular focus on price as the sole defining factor in determining the public interest.

The CRTC, and the federal cabinet, recognized the need to “appropriately balance the objectives of the wholesale services framework”, and acknowledged that the 2019 rates would “undermine investment in high-quality networks”.

The CRTC, and Cabinet recognized that quality, coverage and price work together as public interest considerations. Expanding service to unserved or underserved areas needs private sector investment.

These factors impacting consumers, and the tension between them, show the complex nature of the public interest.

Politicians need to consider the multi-dimensional considerations associated with consumer interests. Consumers have demonstrated that purchase decisions are more sophisticated than simply looking at price.