In his remarks to the National White House Conference on Small Business in 1986, Ronald Reagan said “Government’s view of the economy could be summed up in a few short phrases: If it moves, tax it. If it keeps moving, regulate it. And if it stops moving, subsidize it.”

“Tax it, regulate it, subsidize it” comes to mind when I look at how we seem to be approaching too many elements of Canada’s digital economy.

Last Friday, I read an opinion piece in the Wall Street Journal written by former FCC Chief Economist (and current professor of Economics at Clemson) Thomas Hazlett, “A Lesson for Today’s Tech Trustbusters”. In it, he writes of the angst caused by the $183B acquisition of Time Warner by AOL in 2000.

Regulators feared AOL’s acquisition of Time Warner would stifle innovation. University of Michigan economist Jeffrey MacKie-Mason, who wrote the Federal Trade Commission’s report, said that the combination “will horizontally and vertically increase AOL’s power in the market for internet online services,” which would have anticompetitive effects and harm consumers.

As Hazlett notes, executive mismanagement and clashing corporate cultures are generally cited as reasons for the failure of the merged companies, “But the episode holds lessons for politicians and antitrust regulators, who too often view market rivalry too narrowly.” His article describes the regulatory measures to force AOL to open up its instant messaging platform and how it was quickly superseded by technology. “Texting, Skype, FaceTime, WhatsApp, Facebook Messenger, Twitter and Instagram displaced AOL’s chatting program. None of these new entrants connected with Instant Messenger, or one another, and it didn’t seem to matter.”

Hazlett also notes that this example was hardly isolated. “In 2005 the Bush administration prevented Blockbuster from acquiring Hollywood Video on antitrust grounds: The merger would threaten to monopolize video rentals.”

Consider what is happening in Canada. Recall the CRTC’s interventions into how streaming services Crave TV and Shomi should be offered to consumers? Was regulatory action required or couldn’t the marketplace figure it out?

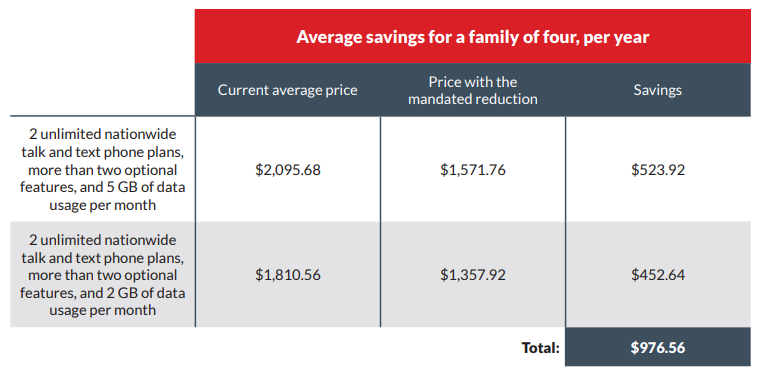

Why is the CRTC continuing to interfere with service providers seeking to lower monthly device payments for consumers? As I have written before, some aspects of the Wireless Code raised the monthly cost of mobile and removed an important choice from consumers.

What purpose is actually served by limiting device amortization to 2 years?

Customers can still switch at will anytime during the contract period. They just have to pay off the balance owing. With higher device costs, people have hefty balances owing anyway, whether it is a two or three year contract.

Eliminating the regulatory restriction on longer contracts could lead to carriers offering direct consumer incentives to switch: “Come to us and we will pay up to $600 of your remaining balance.”

Once the Commission allowed consumers the right to leave a carrier by simply paying off the remaining balance, what purpose is served by the further regulation of how long the amortization period could be?

If the CRTC gets out of the way, surely the marketplace can solve the challenge of consumers wanting to switch service providers before their payments are complete. If new entrants find it tough to lure customers away, they can always pay off the device balance for the new customer and take over the loan. Was there sufficient evidence of a failure in the marketplace to develop a solution before the CRTC intervened so dramatically to remove the choice of a longer amortization period?

Last week, I wrote “Hindsight may be 20/20, but as so many investment prospectuses warn, past performance is no guarantee of future results.”

When we develop policies, we need to resist politically expedient routes and think 3 moves ahead, playing the game more like a chess master than a novice. Communications policy issues are complex and often benefit from looking at secondary and tertiary impacts, trying to contemplate unintended consequences.

As Hazlett has written, there are lessons to be learned from looking at market rivalry or defining the market too narrowly.

“Tax it, regulate it, subsidize it.”

You don’t need to look very hard to see how so many elements of Canada’s digital economy strategy fall into one or more of these categories.

Can we consider a better approach?

Twice before, I have written posts entitled “Getting out of the way” [July 9, 2012 | April 6, 2016]. I wrote another entitled “Keeping out of the way”.

I continue to think “the future will be brighter for Canadian innovation if the government would try harder to get out of the way.”