Homes with tails

Derek Slater and Tim Wu have released an interesting paper called Homes with Tails [ pdf 206KB]. The paper examines consumers taking ownership of their connectivity to the network. Peter Nowak at CBC quoted me in an article about the concept.

pdf 206KB]. The paper examines consumers taking ownership of their connectivity to the network. Peter Nowak at CBC quoted me in an article about the concept.

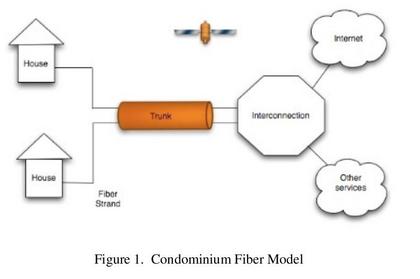

We call this property model “Homes with Tails,” for the fiber would form part of the property right in the home. Key facets of our approach include:1. A “condominium” model for fiber ownership, in which individual strands of fiber are sold to consumers, while maintenance and other collective needs are managed jointly.

2. Private firms and municipalities could consider selling fiber connections based on this model; and

3. Governments could consider using various mechanisms to support consumer purchases, including a tax credit to homeowners or renters who purchase a broadband connection.

It is an early version of the paper and hopefully the authors will continue their thinking and development of the concepts. I’m left not convinced that we’ll see homes with tails outside niche community applications.

Here are some thoughts, in no particular order:

- One of the reasons that traditional service providers have typically shunned delivery of their service over other people’s infrastructure has been the issue of trouble resolution. Consumers typically want one throat to choke and that neck usually belongs to the service provider – the folks charging the end user. If a third party manages the fibre access, how do all of the stakeholders most effectively work through the finger pointing? How much longer will the average repair take?

- Speaking of repairs, the Ottawa experiment is described in the CBC story as having fibre hanging from street-side poles. Anyone who has experienced a winter in our nation’s capital will understand why major service providers are nervous about signing on to a project using aerial cable.

- Will adding a third party access facility manager mean that a new participant is going to have their hand extended for a share of the profit? That means the homeowner is paying thousands of dollars up front for the fibre and a monthly ‘condo fee’ as well.

- Do enough homeowners want to buy such a physical asset or do they prefer to pay for services? Do you rent your water heater or own it? Do you rent your set-top box or own it? What factors went into your decisions on these items? If you are a property renter, what are the implications of your landlord owning your “tail.”

- It might be interesting to examine some of the overall economics associated with the creation of a virtual monopoly in fibre access. For example, what is the impact on a business arranging for a more survivable access architecture, if the condo group has pulled away most of the business case for building metro access facilities?

I found a quote in the CBC article interesting:

The retail internet business in Canada has been destroyed. All you’ve got left in Ontario is Bell and Rogers.

This statement is troubling, especially attributed to CANARIE, Canada’s advanced network organization. In fact, there are lots of retail alternatives operating throughout Ontario and the rest of Canada. They even have an association: The Canadian Association of Internet Providers (CAIP). In fact, when CAIP filed its CRTC application last April, it did so “on behalf of those of CAIP’s members that provide retail Internet access services,” so there should not be any confusion about retail alternatives. There are many others that are not members of CAIP, some of which co-locate and power leased copper loops.

If the concern is that the supply of facilities-based alternatives is too limited, why should we think we are better off with a monopoly condominium fibre manager?

Update [December 4, 1:40 pm]

Derek Slater will be appearing at The 2009 Canadian Telecom Summit in June to talk about Building Broadband networks.

Technorati Tags:

homes with tails, Tim Wu, Derek Slater, FTTH, CAIP, CANARIE, CBC, Peter Nowak