I thought it might be helpful for understanding EBITDA to look at why margins are higher in certain capital intensive industries.

EBITDA is short for Earnings Before Interest, Taxes, Depreciation and Amortization. It is considered to be a proxy for cash flow due to adding back Depreciation and Amortization, but it does not represent net profit, since the business has to pay for its own investments somehow. In capital-intensive businesses, interest, depreciation and amortization can be pretty substantial amounts.

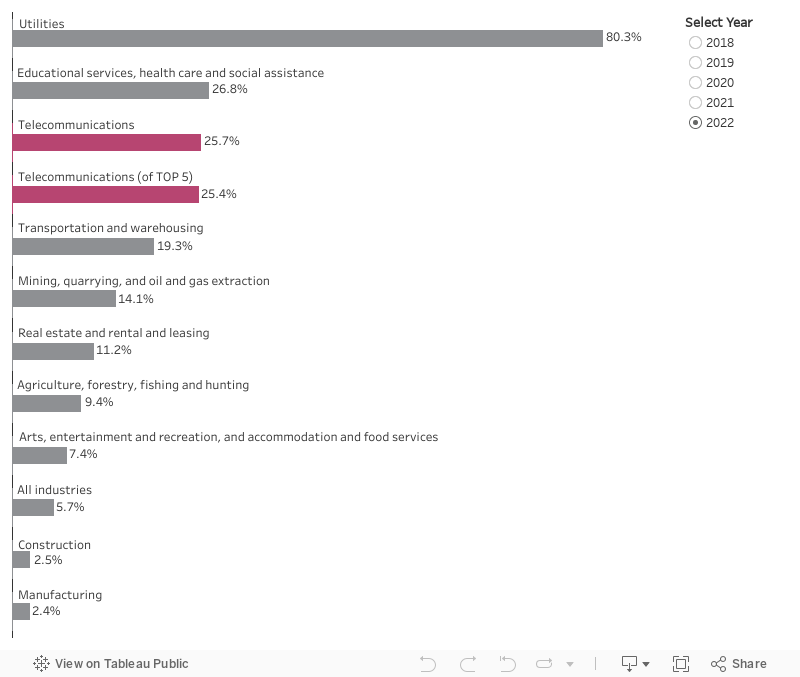

The CRTC’s recent CMR summary included a chart that compared capital intensity across various industrial sectors. Notice that capital intensity (the ratio of capital expenditures to revenues) in telecommunications ranks near the top of all of Canada’s industries. Around 25 cents out of every dollar in revenue is invested by Canada’s telecommunications carriers.

Warren Buffet of Berkshire Hathaway has a well known disdain for EBITDA as a measure of corporate performance. Those who cite EBITDA margins as evidence of excessive profits fall into what Buffet has phrased as thinking “The tooth fairy pays for capital expenditures”. Understanding EBITDA margins, and why this figure varies between capital intensive businesses and those that are less investment intensive, is key to analysing the telecom sector.

Wholesale-based service providers, companies that are reselling carrier infrastructure, have a higher proportion of their network facilities paid for in monthly leases, an expense that is recorded above the line. Carriers, the companies that invest in major telecom infrastructure, need bigger operating margins in order to pay for their investments – those payments recorded below the line resulting in interest, depreciation and amortization. Facilities-based service providers invest in connectivity and long-haul facilities and pay billions of dollars for spectrum, the radio frequencies that power wireless communications.

Those investments require real cash, funds that are not paid for by the tooth fairy.

Keep that in mind the next time you look at EBITDA margins in the telecom sector. Understanding EBITDA means understanding that capital intensive businesses necessarily have higher EBITDA margins.

If I’m not mistaken, the telcos insist on reporting EBIDTA in their annual reports instead of PBIT or some other net income metric. The capital reinvestment levels are very high, but we can’t have a sane public discussion about telco profitability and corporate concentration if no one knows about it.