Many of the headlines last week talked about the CRTC’s 10% interim reduction on wholesale internet rates as part of the Commission’s Notice of Consultation for its latest review of the wholesale internet access framework. The bigger impact story may be in the CRTC’s preliminary view that access to FTTP (fibre to the premises) over aggregated wholesale HSA (high speed access) should be mandated on a temporary and expedited basis, “until the Commission reaches a decision as to whether such access is to be provided indefinitely.”

This was a significant reversal of long standing CRTC policy.

The temporary and expedited nature is noteworthy. After all, let’s say the CRTC, following an evidentiary-based proceeding, reverses its “preliminary view” and decides that its long standing policy was indeed correct, that aggregated access to the FTTP networks could harm incentives to invest in extending FTTP to additional communities. How will the CRTC reverse this temporary and expedited order? Does anyone think the CRTC would actually order companies to reverse these customer connections?

How does that genie go back in the bottle?

In a note to investors about last week’s Decisions and Notice of Consultation, Bank of America wrote:

This wholesale HSA review was anticipated. The outcome could take over a year to complete. We believe it is likely to result in lower wholesale rates and increased access to fiber-to-the-home (FTTH) through an aggregated HSA model where independent ISPs connect to a central point of interconnection to access the facilities-based provider’s entire operating territory (transport and last mile). We think the key will be at what rates. Any incremental reduction to the existing rates helps wholesales. Small changes should help wholesales and have a minimal impact on investment. The risk for the CRTC is overshooting. If rates are set too low, incremental network investment will suffer and consumers’ long-term interest will be harmed. After an impressive multi-year industry investment in fiber, the industry’s ROIC is down materially from five years ago. In our opinion thoughtful regulation will consider the returns such a substantial investment requires (above the cost of capital) to avoid destroying value while encouraging ongoing investment. The industry has a good track record of balancing the demand of shareholders, subscribers, the regulator, and policy makers.

With last week’s Telecom Decision CRTC 2023-53, the CRTC flip-flopped once again on its policies regarding aggregated versus disaggregated wholesale internet access.

Let’s start by defining those terms. Wholesale-based internet service providers (ISPs) resell a portion of a facilities-based telecom service provider’s network. As the CRTC described them in 2015:

- Aggregated wholesale HSA service provides competitors with high-speed paths to end-customers’ premises throughout an incumbent carrier’s entire operating territory from a limited number of interfaces (e.g. one interface per province). This path includes an access component, a transport component, and the interface component. The inclusion of the transport component enables competitors to provide their retail services with minimal investment in transmission facilities.

- Disaggregated wholesale HSA service would provide competitors with high-speed paths to end-customers’ premises served by an ILEC central office or a cable company head-end through a local interface at the ILEC central office or cable company head-end. These paths include an access component and the interface component.

Obviously, it is a lot easier for an ISP to get up and running with just one connection to the telecom service providers. On the other hand, the wholesale-based ISPs have said they can add more value and product differentiation by connecting closer to their customer. However, in its October 2020 intervention in the CRTC’s consultation examining network configurations for disaggregated wholesale internet access, CNOC complained about the cost of connecting to all of the central offices or head-ends.

Since at least 2010, ISPs have promised to climb the ladder of investment. The CRTC and Competition Bureau have each endorsed policies that maintain incentives to promote investment in telecommunications facilities.

Unfortunately, the preliminary view of the CRTC in its Notice of Consultation will see ISPs climbing down that ladder, heading in the wrong direction.

Let’s look at the history of moving back and forth between aggregated and disaggregated wholesale internet access.

- On – Requested by Teksavvy in 2009/2010 CRTC Wholesale Consultation 2009-261: “The problem with the current aggregated services of both the ILECs and the cable carriers is that it forces a lot of the characteristics of those services to be flowed through to the wholesale customers of the ILECs and cable carriers, which really limits the ability of competitors to innovate and offer new differentiated services.” (Counsel for Teksavvy in response to question from CRTC Chair)

- Off – Request for disaggregated denied by CRTC Policy 2010-632: “The Commission is not persuaded that the ILECs and cable carriers should provide new wholesale access services – in the case of the ILECs, an ADSL access service located at the central office, and in the case of the cable carriers, a local head-end-based cable access service. In the Commission’s view, there is no convincing evidence to indicate that there would be a substantial lessening of competition in the absence of these services.” Notably, there is a dissent appended to that CRTC determination, where Commissioner Denton describes disaggregated access as “a technical arrangement permitting significant service innovation, by allowing specialist carriers to differentiate significantly their service offerings from the underlying carrier.”

- On – July 22, 2015 CRTC Policy (2015-326): “the provision of aggregated services will no longer be mandated and will be phased out in conjunction with the implementation of a disaggregated service. Incumbent carriers are directed to begin implementing disaggregated wholesale high-speed access services, in phases.”

- On – May 27, 2021 CRTC Press release: “The existing model, which is an aggregated high-speed access service, is in the process of transitioning to a disaggregated high-speed access service. This will enable competitors to access the fibre-to-the-home networks of the large companies and offer their customers faster Internet speeds and more services for all Canadians… Since 2016, the CRTC’s objective has been to complete the transition to a disaggregated wholesale model for access to the large companies’ high-speed broadband networks. This model will foster greater competition and further investments, so that the industry can better serve the needs of Canadians.”

- Off – March 8, 2023: CRTC Decision (2023-53): “The Commission finds that the disaggregated wholesale high-speed access (HSA) service framework has not fulfilled its mandate and requires reconsideration. The Commission determines that the network configuration for disaggregated wholesale HSA services will remain in Ontario and Quebec pursuant to existing tariffs and will not be introduced in other markets at this time.”

A lot of engineering and regulatory resources were invested developing these wholesale internet access schemes. The importance of consistency and predictability in CRTC determinations cannot be stressed enough, especially in consideration of the capital intensive nature of telecommunications. The new Policy Direction speaks in terms of predictability: “The Commission should ensure that its proceedings and decisions are transparent, predictable and coherent.”

As the CRTC moves forward with its wholesale services consultation, Bank of America said, “the key will be at what rates.”

Last week, I wrote about the difficult tension in seeking increased investment while maintaining, if not improving, affordability. We should measure success in telecommunications competitiveness by how we approach and achieve these often competing objectives: quality, coverage and price.

There is still much work to be done to extend the reach of broadband networks and to upgrade existing facilities. That will require billions of dollars of additional capital investment. That investment is being made by Canada’s facilities-based operators.

For that to move forward, government policies and regulation have to preserve that delicate balance between lowering consumer prices, while preserving incentives for investment to extend and enhance Canada’s high quality networks.

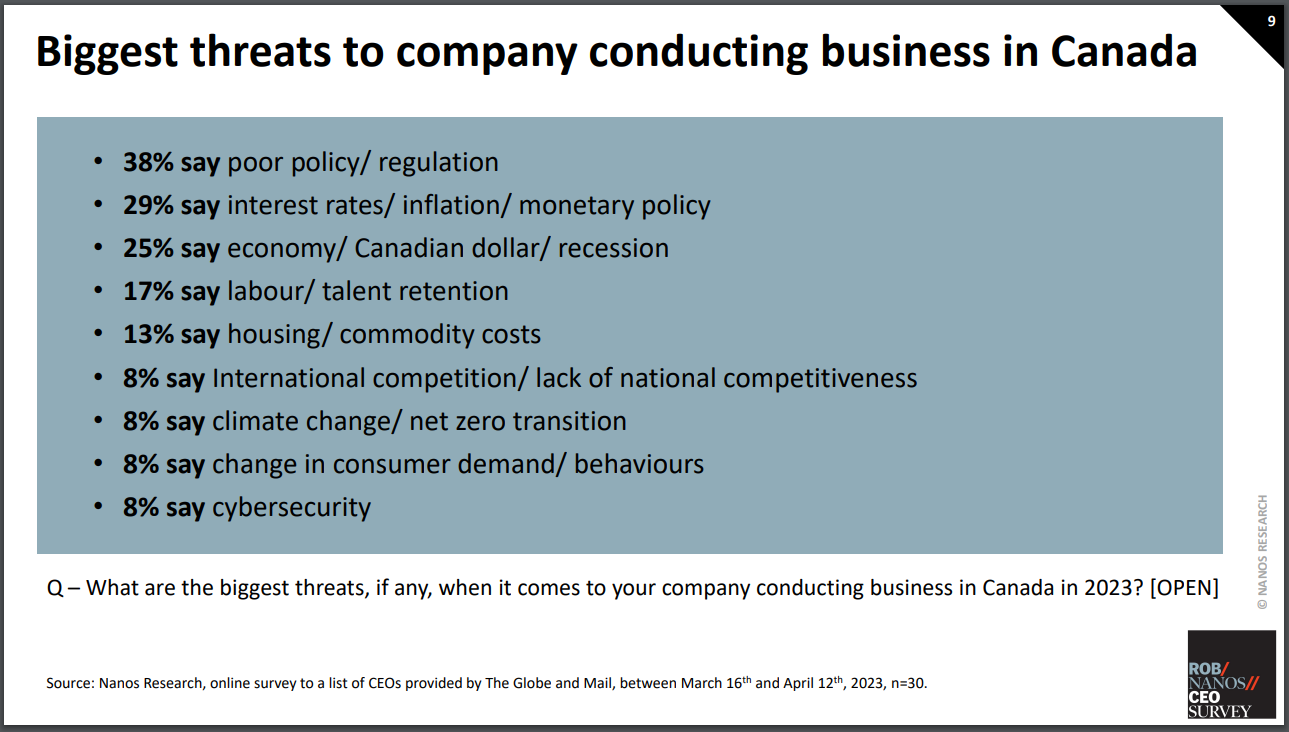

The survey’s headline highlights nine out of ten participating CEOs in Canada see cybersecurity as a threat for their business; 70% say it’s a major threat. Still, Canada being on the wrong track for investment is one of the 4 key findings. “Over six in ten participating CEOs in Canada see Canada as being on the wrong track when it comes to being a place for businesses to invest (62%). When asked the reason for their views, participating CEOs most often said taxes and high costs (22%), poor leadership, regulators, and red tape or lack of clarity (22%), and incentives for business being weaker than other countries which does not create appealing environment for investment (17%).”

The survey’s headline highlights nine out of ten participating CEOs in Canada see cybersecurity as a threat for their business; 70% say it’s a major threat. Still, Canada being on the wrong track for investment is one of the 4 key findings. “Over six in ten participating CEOs in Canada see Canada as being on the wrong track when it comes to being a place for businesses to invest (62%). When asked the reason for their views, participating CEOs most often said taxes and high costs (22%), poor leadership, regulators, and red tape or lack of clarity (22%), and incentives for business being weaker than other countries which does not create appealing environment for investment (17%).” Further, when asked an open ended question “What are the biggest threats, if any, when it comes to your company conducting business in Canada in 2023”, 38% replied poor policy / regulation. It was the number one threat identified, by a nine point margin.

Further, when asked an open ended question “What are the biggest threats, if any, when it comes to your company conducting business in Canada in 2023”, 38% replied poor policy / regulation. It was the number one threat identified, by a nine point margin.