A report from PwC Canada takes a new look at the state of telecom affordability in Canada.

According to “Understanding the affordability of wireless and wireline services in Canada” [26-page pdf, 7.7MB] focuses on assessing three elements of Canadian telecommunications affordability:

Canadian economics statistics, including telecommunications expenditure, inflation, and changing incomes.

The assessment of wireless and wireline affordability in Canada, including assessing the changing prices of wireless and wireline services over time relative to increases in data consumption and changing patterns of data usage.

The affordability of wireless and wireline services for Canadians against consumption and income metrics relative to global jurisdictions.

What did PwC find?

Canadians have been impacted by inflation, with inflation in 2021 and 2022 surpassing the rate of income growth. Prior to 2021, incomes were growing faster than inflation for every quintile except the highest.

Between 2017 and 2021, cellular services was the second largest CPI drop among the only 13 deflationary goods and services in the CPI bucket, falling at a CAGR of 8.1%. Driven by the decrease in cellular service CPI, communications was also a deflationary service, with communications CPI falling by 16% from 2017 to 2022.

Affordability increased for all quintiles when assessing the cost of entry-level wireless and wireline plans against adjusted disposable incomes. Notably, for the lowest income quintile, the affordability of entry-level wireline plans improved by 11% between 2017 and 2021, while wireless affordability improved by 39%.

The price per gigabyte of wireless and wireline data fell by over a 19% CAGR in Canada from 2017 to 2021. This is attributed to increases in data consumption significantly outpacing changes in prices, with data consumption growing at CAGRs of 24% for wireless and 28% for wireline. Among selected international peers, Canada has the second-lowest cost per gigabyte of wireline data.

The affordability of wireless and wireline services in Canada is on par with peer countries. As the CPI of Canadian communications has dropped, it has brought the price of services in line with international peers as a percentage of income, indicating relative affordability.

Together, the Canadian market and international analyses demonstrate that facilities-based competition in Canada is able to maintain a healthy telecommunications industry while delivering on network coverage, quality, and affordability

Earlier this year, I wrote, “Affordability is a complex and multifaceted concept that varies depending on the context and the goods or services being considered.”

The report looks at telecom affordability across various income quintiles, but it did not explicitly include a discussion of targeted affordable services such as the industry-led Connecting Families initiative. It is worth noting that Rogers recently introduced its Connected for Success 5G Wireless Program, promised as a benefit of the Shaw acquisition, and it has rolled out its broadband Connected for Success to the former Shaw footprint. TELUS offers Mobility for Good, among other targeted services, as I have described.

The PwC report lays out a fact-based narrative on telecom affordability in Canada, and paints a very different picture from the conventional wisdom.

Could the CRTC’s latest wholesale regulations stifle competition, precisely the opposite of what was intended?

The introductory section of the decision is filled with puzzling statements, like this:

In recent years, the Commission has noted declining competitive intensity in this industry. The number of Canadians who buy Internet services from independent wholesale-based competitors has fallen by 40%, even as the overall number of Internet subscribers in Canada has increased. In addition, a significant number of wholesale-based competitors have been bought by incumbent companies. When competitors exit the market, Canadian consumers are left with fewer options. It is therefore important that the Commission revise its approach to promote competition and protect the interests of Canadians.

The CRTC seems to believe that the most relevant measure of competitive intensity is by counting the number of smaller wholesale service resellers. The CRTC didn’t look at pricing as a measure of competitive intensity; despite rampant inflation, prices for internet services have declined nearly 8% in the past year according to Statistics Canada’s Consumer Price Index. The CRTC didn’t look at levels of investment; a recent PwC report found “the Canadian telecom sector has invested an annual average of $12.1 billion in capital on network infrastructure. This represents approximately 18.6% of average revenues, which is higher than the 14.2% average across the peer telecoms in the U.S.A., Japan, Australia, and Europe.”

Falling prices and high levels of capital investment are inconsistent with declining competitive intensity.

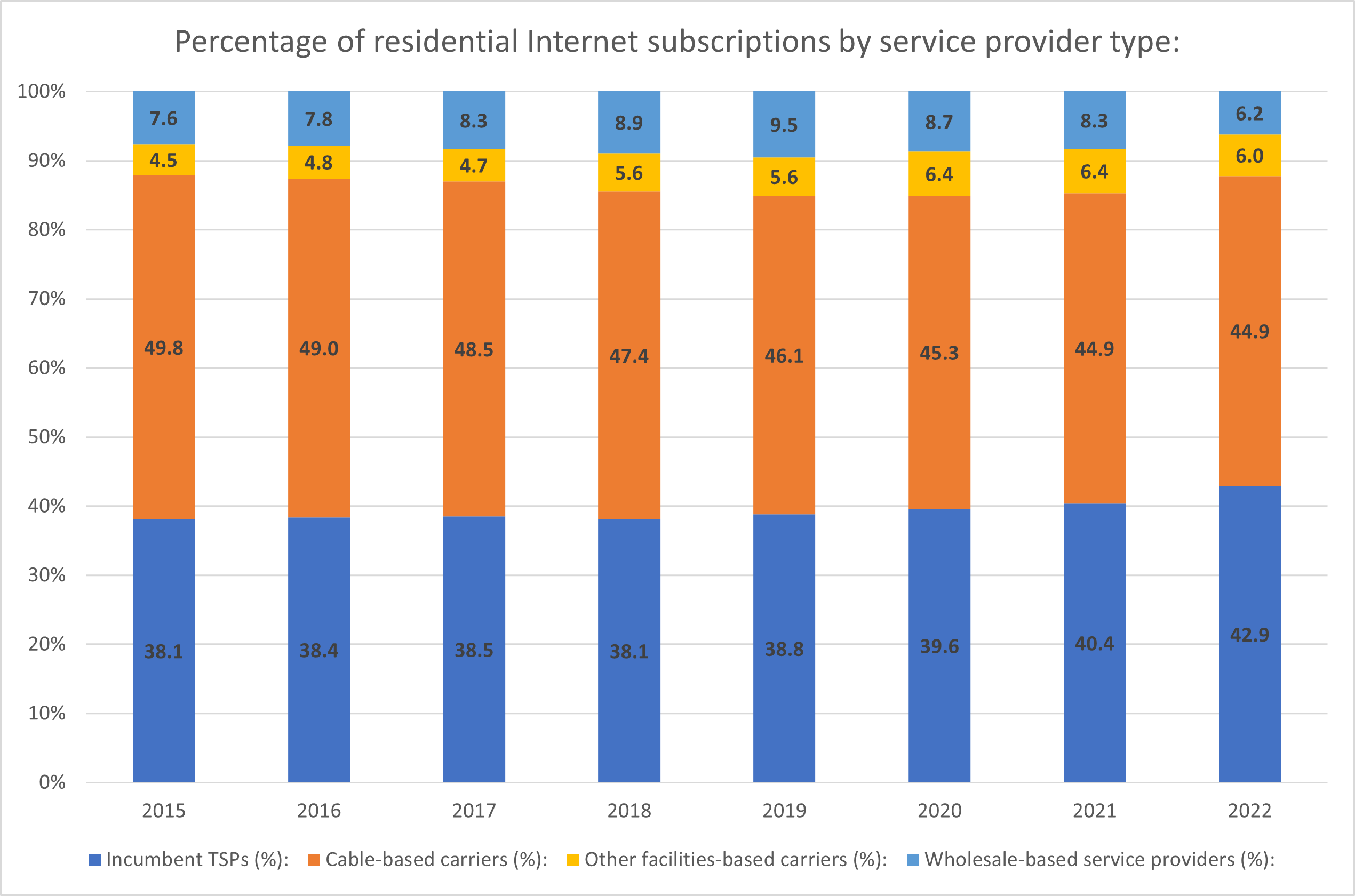

The CRTC claims there has been a 40% drop in the number of Canadians who buy internet services from “independent wholesale-based competitors”. (I am unable to find data that supports the CRTC’s 40% drop in wholesale subscriptions. The CRTC’s Open Data shows that wholesale subscriptions fell 30% from a peak of 1.3 M in 2019 to 0.9 M in 2022.) In any case, this is a small subset (roughly 6%) of the competitive marketplace for broadband services. Let’s look at the CRTC’s own open data (Tab N-I5 of the Data – Retail Fixed Internet table). This chart examines the share of the residential internet market by type of service provider.

What we see is that phone companies (termed “Incumbent TSPs”) and cable companies jointly held 87.9% of the market in 2015. That share declined each year through 2020, before moving up slightly in 2021. Newly released 2022 data shows a 2.5% jump in phone company share, largely at the expense of wholesale-based service providers and likely due to acquisitions. The independent wholesale-based segment dropped in 2022 by 2.5% of the market to end the year with 6.2% share. I’ll note that in most cases, the acquired companies continue to operate as flanker brands, so consumer choice has not been reduced.

What is interesting to see is the relatively steady growth in the segment called “Other facilities-based carriers”, rising from 4.5% to 6.0%. Other facilities-based carriers have grown their market share, going from 700,000 subscribers in 2018 to 900,000 in 2022. In other words, we are seeing evidence of the success of facilities-based competition.

The CRTC’s remedy for the declining presence of one type of market participant (wholesale-based) is to require Bell and TELUS to enable resale of their fibre to the home facilities in Ontario and Quebec only. Why Ontario and Quebec only? The CRTC Decision says “The record of this proceeding shows that the competitive presence of wholesale-based competitors has declined most significantly in Ontario and Quebec. These provinces are where competitors have historically attracted the largest number of subscribers, and where they are currently losing subscribers the fastest.”

Duhh. Of course these two provinces “have historically attracted the largest number of subscribers”; more than 60% of Canada’s population live in Ontario and Quebec. Doesn’t it follow that these provinces are where competitors would attract the largest number of subscribers? And it logically follows that where you have the most subscribers would correspond to where service providers would be losing subscribers the fastest. If the CRTC wants to change that state, why is the decision geographically limited? As the CRTC explains in the body of the decision, the Commission still isn’t sure if mandated wholesale access is going to be a permanent or temporary arrangement. “[T]he Commission considers that a narrower scope would reduce the potential impact on both competitors and the incumbent carriers if the Commission later determines that aggregated FTTP access is not required on a longer-term basis or is to be provided under different service configurations.”

In any case, the decision applies only in Canada’s two largest provinces and only to the two largest phone companies, not the cable companies and not the independent phone companies, such as TBayTel in Thunder Bay. In reality, this means the decision has a disproportionate impact on Bell because TELUS is the incumbent local phone company for a much smaller share of the total population, and only in Quebec. But it is worth noting that the cable companies, not the phone companies, are the biggest segment in the broadband market. Resale of gigabit services from the cable companies have been mandated by previous CRTC determinations.

In last week’s decision, the CRTC claims it recognizes and is supportive of investment in facilities.

At the same time, the Commission recognizes that continued investment by incumbent companies is crucial to ensuring that Canadians continue to benefit from robust and reliable Internet services. To achieve this, the Commission has established just and reasonable interim rates that wholesale-based competitors will pay those incumbent companies for access. These rates will ensure that large incumbent companies across Canada continue to have incentive to invest in their networks.

Unfortunately, just and reasonable rates for existing fibre facilities don’t necessarily support the business case for building fibre in new areas.

Even though the wholesale rate may be set to cover the “cost” of the facility, Bell won’t be financially indifferent when a customer chooses a resale-based service provider. Scotiabank estimates that FTTH households have an average $140 per month bundle, substantially more than the revenue associated with a wholesale customer. A major inhibitor of new fibre construction is that the CRTC rejected Bell’s proposal to base the rates on a combination of 5 years of historical and 5 years of forecasted capital. The CRTC set rates based on the historical capital costs.

As Scotiabank recently noted, the average cost per home for fibre has historically been in the order of $1500. This is expected to increase to $2000 per location as fibre plans move to less urban locations. These areas may already have a cable company providing 50/10 broadband and therefore are ineligible for government broadband subsidies. So phone companies look at whether the expected revenues from expansion justify the cost of upgrading to fibre in order to compete against the cable company. With higher capital costs to roll out fibre to less-urban households, the revenue requirements are logically higher. In any business, if the expected revenues from a proposed fibre area don’t provide a reasonable return on the investment, the capital project won’t get approved.

As a result, Bell responded by announcing a cut in its capital program. The capital cuts won’t impact the urban centres; those areas already have fibre. The budget cuts likely will not impact fibre rollout to areas that do not have 50/10 broadband, although there may now be a larger subsidy requirement. As I have written before, the biggest areas of concern will likely be in suburban areas, where the business cases for fibre is most fragile.

I can’t help but consider the irony of the CRTC’s wholesale fibre decision resulting in a reduction in facilities-based competition, the competitive choice of more than 90% of all Canadians.

Is the CRTC choosing to protect competitors when it should focus on protecting competition? Does the most recent decision micromanage some industry participants, attempting to support one group of competitors at the expense of others? To what extent should the CRTC be examining factors to incent intermodal competition for consumer broadband, leveraging 5G for fixed wireless?

The Commission needs to carefully consider whether its regulations stifle competition, and inhibit investment.

Many of us have come to expect constant connectivity.

I don’t mean we necessarily want to be online 24/7, with a screen in front of our face around-the-clock. But, we want to be able to be connected whenever we want, wherever we happen to be.

Constant connectivity.

Most of us have phones that are effectively able to serve as mobile offices, equipped with word processing and other business apps. Personally, I find spreadsheets painful to navigate on my 5-inch screen, but I frequently edit blog posts and documents from waiting rooms or restaurants. We have tablets, computers, smart TVs, smart speakers, thermostats all connected to our home internet. As I write this, my home router reports 33 devices are connected. (I don’t have many of the “smart home” devices that are increasingly commonplace).

On our mobile networks, in addition to our smartphones, we have metering and other forms of telemetry. With home security and health applications, we increase the need for reliability, often using wireless backup for wireline connections. There are many working groups talking about connected autonomous vehicles.

This state of constant connectivity carries with it a variety of implications.

Many applications can be designed to tolerate hiccups in their connections. For example, by their very nature, email messages are transmitted on a ‘store and forward’ basis. A delay measured in tens of seconds or even minutes or hours is somewhat meaningless for most messages. It is silly to be concerned about a sub-second delay for emails or most text messaging. Most streaming video applications are designed to buffer the signal, storing multiple seconds of content on your device in anticipation of possible interruptions. But, what about voice and two way video calling? Delays (latency) of more than a few hundred milliseconds can be challenging for many who are used to virtually instantaneous responses in a normal conversation. We can witness the uncomfortable user experience when foreign news correspondents are having on-air communications with anchors using satellite connections.

What about performance issues with applications requiring non-stop high performance connectivity, such as remote surgery?

Connected vehicles is a category that enables us to understand a wide range of performance requirements, just in connecting a car. What kind of network performance should be anticipated by developers of connected car applications? The performance characteristics will vary based on whether the connectivity is used for navigation, entertainment, diagnostics, accident avoidance, or telemetry for vehicle maintenance (among other applications).

For many applications, constant connectivity may not have to be quite so constant.

Over the past few years, I have frequently referred to the tension between quality, coverage and price in architecting networks. Increases in coverage, or improvements in performance are always possible, but there is a cost associated with each. That cost ultimately would need to be recovered.

Do regulation and policy recognize that not all bits need to be treated the same?

How should variances in technical requirements receive consideration when examining network resilience from a regulatory perspective?

How do we ensure that appropriate incentives are in place to encourage continued investment in networks for improved reach, robust network resilience, increased capacity and more advanced capabilities?

In 2022, Canadian carriers were investing in telecom infrastructure at an accelerated pace.

That is one of the findings of a new report prepared by PwC. “Connecting Canadians through resilient networks: The impact of the telecom sector in 2022 and beyond” [pdf, 4.5MB] found that Canada’s six largest telecom companies invested $13.3 billion in capital expenditures in 2022. Over the past five years, the Canadian telecom sector has invested an annual average of $12.1 billion in capital on network infrastructure, expanding, enhancing, and strengthening Canada’s wireless and broadband networks. This represents approximately 18.6% of average revenues, which is 30% higher than the 14.2% average across peer telecom carriers in the US, Japan, Australia, and Europe. Canada’s elevated capital intensity is similar to what was found in another recent study.

As I have reported in my monthly analysis of Statistics Canada data, PwC confirmed that for the year ending September 2023, cellular and internet access service prices declined by 17.2% and 7.8%, respectively, while the Consumer Price Index for All-Items increased by 3.8% over the same period.

PwC says the telecom sector contributed nearly $77B to Canada’s GDP, and supported nearly three quarters of a million Canadian jobs in 2022. It estimates that by 2035, the telecom sector’s delivery of enhanced connectivity, including 5G, has the potential to contribute an additional $112B to Canada’s GDP.

Key findings:

Direct GDP contribution and jobs supported by the telecommunications sector in 2022 is estimated to be $76.7 billion and 724,000 jobs (versus $74.9 billion (+2.4%) and 650,000 jobs in 2021 (+11.3%)*);

Enhanced connectivity, including 5G, has the potential to contribute an additional $112 billion to Canada’s GDP by 2035

Telecom’s direct GDP contribution includes $24.7 billion from the sector’s value chain and up to $52 billion in direct impact from increased sales and other outputs from other Canadian industries through the incremental addition of additional wireless and broadband connections;

The six largest Canadian telecommunications operators invested $13.3 billion in capital expenditures in 2022 to continue expanding and enhancing their wireless and broadband internet networks;

Over the past five years, Canada’s telecom sector has invested an average of $12.1 billion annually on network expansion and enhancements. This represents a capital intensity that is approximately 18.6% of average revenues. That is higher than the 14.2% average across peer telecom operators in the US, Japan, Australia and Europe;

Continued investments in Canada’s telecom sector connect more Canadians to advanced wireless and broadband internet networks, supporting increased data consumption, powering the digital economy, and providing a range of other social and environmental benefits:

99.7% of Canadians had access to mobile network coverage where they lived or conducted business in 2021, including 87.8% who had access to 5G connectivity;

93.5% of households had access to high-speed internet with speeds meeting the CRTC’s 50/10 Mbps targets in 2022. The CRTC estimates that services providers are on track to meet its broadband targets for 98% of households to have access to 50/10 Mbps unlimited services in 2026, and 100% by 2030;

The price of telecommunications in Canada has fallen over the past year, with cellular service prices down 17.2% and internet access service prices down 7.8% between September 2022 and September 2023, while the all-items Consumer Price Index increased by 3.8%;

The telecommunications sector has already suffered millions of dollars in damages to Canadian network infrastructure as a result of severe weather events and other natural disasters. Canadian service providers are investing in building resilient networks to manage future risks.

The bottom line? Maintaining incentives for investing in telecom infrastructure is key to Canadian economic growth.

STAC 2024 brings together the people who physically construct Canada’s telecommunications networks. As I have written before, I have frequently been jealous of people who work in construction. At the end of a shift, those workers can see what they accomplished. That is a huge advantage over the kinds of longer range jobs that I have had.

The event is dedicated to tower safety in Canada. The annual STAC conference is a vibrant forum for sharing crucial insights and best practices that are vital to maintaining Canada’s renowned tower safety record. Located at Vancouver’s downtown Sheraton Wall Centre, STAC 2024 is expected to unite more than 300 professionals from across Canada’s communications and tower industry, spanning wireless carriers, broadcasters, engineers, contractors, manufacturers, landowners, safety equipment suppliers, and safety trainers, among others.

We have clearly seen the essentiality of these dedicated telecommunications professionals:

as the communications industry continues to extend service to rural and remote areas;

communications services providers reinforce network resilience in the face of changing weather patterns; and

carriers enhance and expand 5G networks in urban, rural and private applications.

STAC 2024 represents an opportunity for them to convene, interact, celebrate successes, and learn from each other.

STAC and the STAC 2024 Conference & Exhibition are administered by the Canadian Telecommunications Association, which is dedicated to building a better future for Canadians through connectivity. Through its advocacy initiatives, research, and events, the Association works to promote the importance of telecommunications to Canada’s economic growth and social development and advocate for policies that foster investment, innovation, and positive outcomes for consumers. In additiona to STAC, the Association also facilitates industry initiatives, such as the Mobile Giving Foundation Canada, Canadian Common Short Codes, and wirelessaccessibility.ca.