The WIND Mobile – Shaw deal should make Canadians re-think the way we refer to the communications industry. I’ll let you read other accounts of the business aspects of the transaction, such as what you will find in the Globe and Mail.

As always, I like try to help you look at these things from a different angle.

Consider the usual shorthand that is used for the industry. In the wireless business, we often talk about Bell, TELUS and Rogers as the Big Three, or the incumbents. All the others are captured under the collective term “New Entrants”. As early as the 2007 AWS auction rules, the government has distinguished between Bell, TELUS and Rogers, and the rest of the industry. Of course, the government doesn’t refer to “the Big Three” or use the corporate names. It refers to New Entrants as “An entity, including affiliates and associated entities, which holds less than 10 percent of the national wireless market based on revenue.” Who has 10% or greater? Bell, Rogers and TELUS.

We use the magic 10% elsewhere, when looking at companies eligible for foreign control. In that instance, Section 16(2) of the Telecom Act allows foreign control if “it has annual revenues from the provision of telecommunications services in Canada that represent less than 10% of the total annual revenues, as determined by the Commission, from the provision of telecommunications services in Canada.” Right now, Bell, TELUS and Rogers are the only telecom operators with revenues that exceed such a floor.

So the terminology is perhaps useful shorthand from a legislative and policy perspective, but less so for consumers.

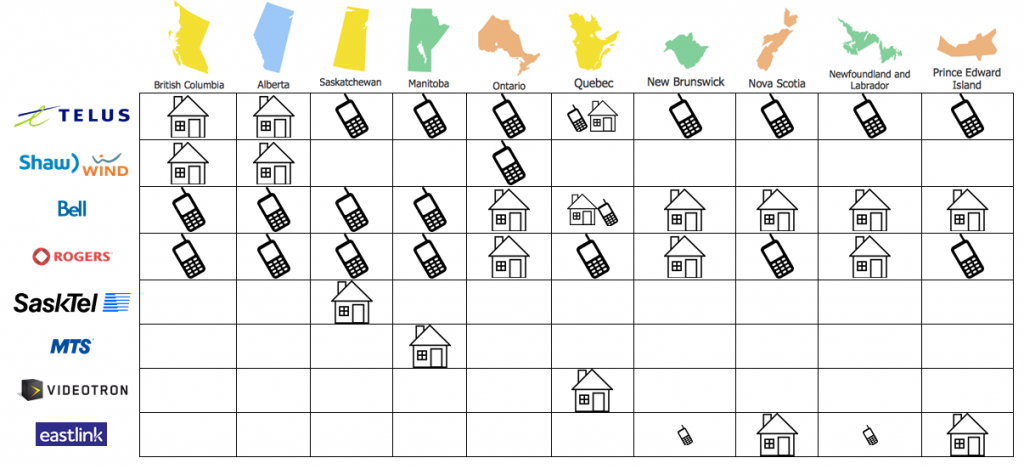

Consider Manitoba and Saskatchewan. MTS and SaskTel, at more than a century old, are considered a “new entrant”, yet those two companies were the only industry participants able to offer a full consumer bundle (TV, internet, wireline and wireless) to the residential customers in their respective provinces. The “Big Three” only had wireless services; Shaw offered TV, internet and wired phone.

In Alberta and BC, TELUS had the ability to offer a full portfolio of services; everyone else had a limited suite. In Ontario, two of the Big Three (Bell and Rogers) could compete for the broadband home, while TELUS, like a “new entrant”, only had wireless. For Quebec and much of the Atlantic provinces, a new entrant (Videotron or Eastlink) offers competition to Bell’s bundle, while Rogers and TELUS take on the role of wireless-only players.

How relevant is a product bundle? There are two aspects: one part is the attraction and stickiness for consumers, perhaps driven by simplicity, by negotiating leverage for package discounts and simplified billing and payments; but there is also an operational savings component, with lower administrative costs, and integrated network savings. There is clearly a benefit to having local network facilities when running fibre connections to wireless towers and new nano-cell architectures can leverage local home broadband connections to improve mibile network coverage.

“Big Three” may be a meaningful term for enterprise business customers looking for national contracts, but most consumers are interested in the level of competition available to them. To that end, the Shaw – WIND Mobile transaction provides an assurance of a stable fulfillment of former Industry Minister Christian Paradis’ objective set out 33 months ago: “our government wants to see at least four players in each market”.

The regional aspect of that objective was frequently forgotten, but it is a very important aspect. When the Shaw – WIND Mobile deal closes, virtually all Canadians will be able to choose wireless services from four players in every market; two of those players with a complete portfolio of broadband home services, and two players having just a mobile offer. In each market, different industry participants have different market positions and therefore will offer different value propositions to attract customers.

That kind of differentiation is good for consumers.

There are four well funded mobile service providers, each with integrated multi-service capabilities in various parts of their operating territories, helping to provide a measure of diversification. Each of wireless companies is associated with a company that has been operating in parts of the Canadian communications industry for decades. This is helpful in an industry that needs annual capital investment measured in the hundreds of millions of dollars to stay ahead of users’ seemingly insatiable demand for more capacity.

Names can be important. The terms “Big Three” and “new entrant” no longer have the same meaning in the Canadian communications marketplace. Similarly, we need to think carefully about what it means to call a service provider an “incumbent”. That will come into play as we examine upon what companies basic service obligations may be imposed. But that can be a discussion for another day.