Succeeding in uncertainty

PwC has released its 23rd annual CEO Survey, entitled “Succeeding in uncertainty” [pdf, 2.5MB].

The report observes that uncertainty is weighing on growth prospects across all industries in Canada:

Entering 2020, Canadian CEOs are more uncertain than ever. In 2018, 72% of Canadian CEOs expected global economic growth to improve, but this optimism dropped to 38% in 2019 and 14% this year. In fact, CEOs are the most negative they have been at any time in the past five years. This finding is compelling because the change in CEOs’ revenue confidence has proven to be a reliable indicator of both the direction and level of global GDP growth in the year ahead.

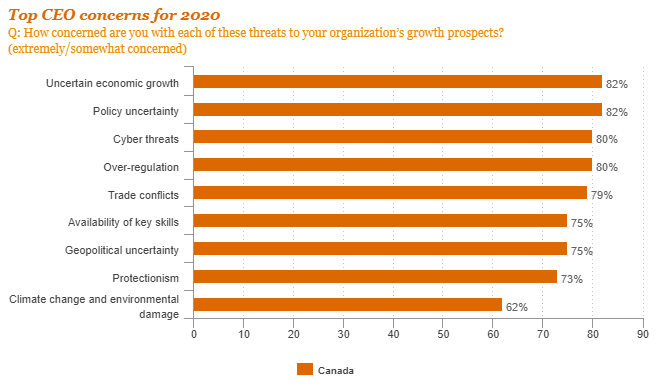

Among the top five concerns identified by Canadian CEOs were a number that should resonate with those following telecommunications. CEOs were asked “How concerned are you with each of these threats to your organization’s growth prospects?” These five areas, each attrated “extremely concerned” or “somewhat concerned” from about 80% of respondents:

- Uncertain economic growth

- Policy uncertainty

- Cyber threats

- Over-regulation

- Trade conflicts

Across all industries, a full 42% of CEOs were ‘extremely concerned” about over-regulation; 38% were somewhat concerned. “Only a quarter of Canadian CEOs say that governments are designing privacy regulations that actually increases consumer trust and that governments and businesses are effectively collaborating to harmonize cybersecurity strategies.”

Three quarters of CEOs have identified concerns about the availability of key skills to match growth prospects.

The survey was conducted in September and October of last year and includes insights exploring the sources of uncertainty and suggesting how CEOs can forge “a path in today’s new world.”