The Government of Canada has been running a series of ads with the tag line: “Less noise. More facts.”, with directions to readers to get more information on a special Industry Canada website.

The Government of Canada has been running a series of ads with the tag line: “Less noise. More facts.”, with directions to readers to get more information on a special Industry Canada website.

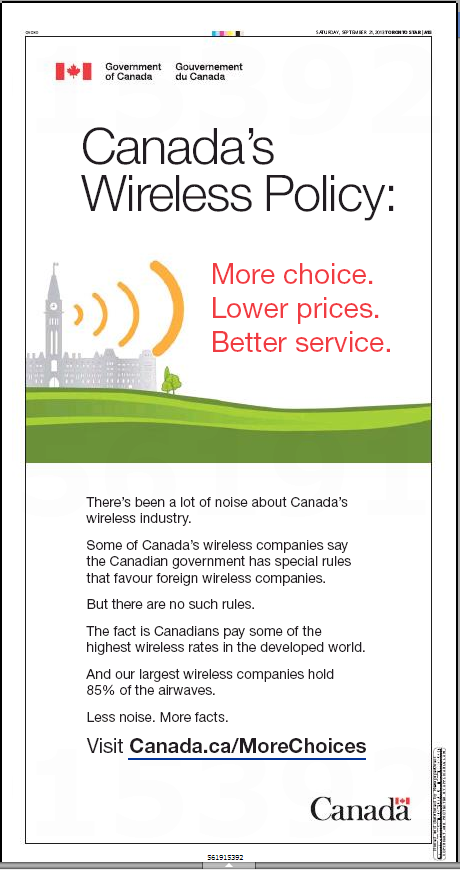

I tweeted earlier this week that I think the campaign is unseemly and sophomoric.

On reflection, I think the government needs to take its own advice and provide less noise and more facts.

There are at least two major points that merit scrutiny.

The ad says “The fact is Canadians pay some of the highest wireless rates in the developed world.”

That simply isn’t true, and the government knows it. Industry Canada and the CRTC commissioned a report [html, pdf] that looked at international pricing; less than 3 months ago, then Minister of Industry Christian Paradis welcomed its release, saying:

Based on Wall Communications’ results, wireless prices have decreased 18 percent since 2008. This impressive decline shows that increased competition is keeping prices down while new technologies become available.

We know that the people responsible for the Government ad campaign are aware of the Wall Communications study; the government cites figures from that report when taking credit for prices dropping by 20%. The Wall Communications report doesn’t stand alone. The School of Public Policy at University of Calgary released a report two weeks ago on Parliament Hill. The report was written by economists who found:

wireless prices in Canada are difficult to compare to international prices because Canadians use their mobile devices differently – with a bias toward monthly plans over pay-as-you-go and with fast networks that encourage smartphone usage. This incorrectly leads to the conclusion that Canadians are paying more, when in fact they are demanding more in terms of mobile services.

The authors of the University of Calgary report are experts in competitive markets, both of them having worked at Canada’s Competition Bureau. As I wrote at the time, The paper takes aim at simplistic analysis that has led various critics to have accused the industry of being “woefully uncompetitive” and “dysfunctional and in desperate need of an overhaul.”

According to their report, “there is no evidence that there is a competition problem in wireless services in Canada.” Yet Industry Canada’s More Choice website ignores this finding. Industry Canada says it is a fiction that “There is already enough competition in the wireless market.”

The University of Calgary report is an inconvenient contradiction – one that cannot be ignored.

As I suggested on Monday, it is time to take stock of where we are. How do we create the right policy framework to encourage the continued investment of billions of dollars each year, delivering advanced, affordable services that enable Canada’s participation in a global digital economy?

I agree with one part of the ads that my taxes paid for. We need less noise and more facts. We can then follow up with thoughtful analysis and leadership.

the public ‘noise’ against high prices was started by the public, the government responded.

just who is the adult in this battle?

I have this question, who reading this blog thinks they aren’t being taken for a ride by the big 3 wireless telecom when they look at their bills at the end of the month?

@JB

I have a vacation home in the US where I pay $48/mo for 1.5 Mbps internet service through Frontier – by today’s standards that’s a very steep price for an anemic service. Even if I was willing to pay more for faster service, higher speeds aren’t even available. In contrast I pay $43/mo for a 25 Mbps service at my home in Canada.

I spend about 4 months a year in the US so I have some first hand experience with their cell phone networks. I haven’t had a dropped call in Canada for at least a year now. In the US, every other call is dropped. Wireless data speeds in Canada are absolutely fantastic whereas wireless data speeds in the US are pathetic – they remind me of the EVDO and GPRS speeds we had in Canada 7-8 years ago.

Since I spend a fair bit of time in the US, I have a subscription with Verizon. My experience is that Verizon’s costs are a little bit higher than what I pay in Canada but the quality of service in Canada is twice as good.

I was in London UK and Paris this past summer. I didn’t see any 4G networks in either of those cities – London was mostly 3G but Paris was mostly 2G and occasionally 3G. These mega-cities are several years behind Canada when it comes to wireless networks.

From my experience we have vastly superior service in Canada at prices that are generally cheaper than the US. My personal experience aligns with the government’s report this past summer that says essentially the same thing – prices in Canada are lower than the US.

Interesting that the Federal Government’s goals are lower prices, but yet they auction their spectrum with the sole goal of getting the most amount possible for it. Post auction, the costs of the spectrum are ultimately charged back to the customers, since there is no spectrum money tree to pay for the spectrum. And then the CRTC in its wisdom decides to effectively outlaw three year contracts. And again the price to consumers goes up since their $700 smartphone now needs to be paid for over 2 years instead of three years. The federal government is totally inconsistent in their policy approaches and is simply playing politics.

poor,poor wireless telecoms, how are they able to pay for spectrum when they only make billions every year! What are they going to do,John? Tsk,tsk,tsk

Mike, I believe that your experience is consistent with many Canadians’. But there are also many of us who have a much more mixed experience.

I live in Manitoba and regularly travel outside Winnipeg for work and pleasure. If I venture slightly off the beaten path I often find myself dropping calls or without enough service to use data or send texts. The situation is particularly bad, as many can attest, in cottage country, where infrastructure cannot handle seasonal peak loads.

In the States, Sprint and T-Mobile offer unlimited data. I’m lucky enough to have MTS service, but as I understand it, our provincial incumbent is the only company in the country offering non-capped wireless service.

John,

I agree that government reliance on revenue raised from auctioning public resources is truly problematic. This is doubly so, if, as I’m correct, the money is funnelled into general revenue and not used for targeted programs, such as rural service subsidization or assistance programs for low-income Canadians.

However, the government isn’t solely to blame, as the telecom industry was ripping off Canadians long before phone calls took to the air.

Here’s a fun experiment: go to a wireless kiosk at your local mall, and ask them how much the handset you want costs. They will tell you the subsidized price. Then ask them: who pays for the rest? Chances are they will tell you it is a gift to you, given in exchange for signing a contract. Of course we all know better, but what we don’t know is how much they’re paying for their phones at wholesale, nor how much of our bills go toward equipment.

It’s a complicated mess, our telecommunications environment. But laying the blame exclusively at the feet of either business OR government (or the public, for that matter) is not constructive.

@Ben

Your experience demonstrates the obvious flaw in the Harper government’s wireless strategy. Manitoba already has four large carriers operating in the province. Yet despite having four large carriers competing for business, Manitoba has some of the poorest service coverage in the country, why? If the PMO’s strategy is correct, Manitoba should have the best coverage and the lowest prices.

The technology to fix the coverage problem is readily available but for some reason all those carriers aren’t committing the capital to do it. Perhaps they are doing what every responsible business does every day – they are investing their capital where they have a decent chance of earning a return on their investment.

This same scenario is unfolding across the EU right now. In late July the EU issued a news release bemoaning the lack of 4G wireless network and highlighting the economic risks to the region for being so far behind on the technology curve. It appears the problem in the EU is too many wireless companies chasing too few customers which drives prices down while simultaneously pushing many carriers to the brink of bankruptcy. With little money coming in, many EU carriers have slashed their spending on network upgrades.

If the PMO continues their ill-conceived wireless competition strategy, rural wireless coverage will be one of the biggest casualties.

I think you’re correct to point out that a strategy reliant on foreign capital investment in infrastructure procurement will not work. (It’s been failing since at least 2008, but arguably since Microcell and Clearnet were absorbed by the incumbents – not sure offhand about their foreign ownership ratios.)

National capital investment has failed to provide relief for Canadians for the same reason. There are alternatives to relying on large-scale private investment in network infrastructure in my opinion.

As you say, any good business owner wants as good as possible a return on their investment. I think part of the problem is that our WSPs are in the wrong business. Ownership of large scale infrastructure is a natural monopoly. It just doesn’t make economic sense to duplicate facilities past a certain point. I think that this points to an alternative that demands serious consideration: open-access networks.

The wholesale regime in broadband internet provision seems to be gaining steam. the CMR shows that “reseller” revenues have been increasing. Some Ontarians by now must be familiar with Teksaavy for their lower prices and un-capped service.

Unfortunately such a regime does not exist in the wireless sphere. Some companies – like 7-11 and PetroCanada have negotiated private agreements with network owners – but the terms so far have not been competitive (Seriously hobbled access to data services, which are clearly in high demand).

A market characterized by many service providers (known as “MVNOs,” or mobile virtual network operators), could go a long way toward bringing prices down for consumers. Efficient, narrowly tailored regulation could achieve this within the current policy framework.I think that this is an option that needs to be explored, rather than continuing to cast out lines, hoping against all evidence that a big foreign fish to bite on.

Natural monopoly? Not sure the evidence supports the assertion that wireless infrastructure is a natural monopoly.

Any economists have views?

Given the context (a blog comment) my characterization was necessarily reductive.

A more nuanced view would have it that the observable limitation of firms’ willingness to make capital investment in infrastructure suggests that the market for networks more closely resembles a monopoly than a perfectly competitive market.

I would place the current state of this market closer to “oligopoly” or at the extreme “monopolistic competition.” My analysis is based on the framework set out by John Strick in “The Economics of Government Regulation.”

I think the problem created by this situation results in a fundamental conflation: service provision and network infrastructure are today part of the same business. Tendency toward concentration in the latter leads to rent-seeking in the former.

But this is not necessarily a necessary feature of functional telecommunications markets; AT&T has indicated interest in moving away from tower ownership/maintenance for instance. Greg O’Brien provided a wonderful illustration of the inefficiencies that result from this practical conflation during his interview on TVO’s “The Agenda” program Thursday night.

In a nutshell, what I’m saying is that facilities-based competition can only take us so far because of the limitations on investment viz. the economies of scale associated with infrastructure markets, and the resulting incentives toward rational rent-seeking on the part of producers. A market structure that separates service provision from facilities ownership represents a superior arrangement from the perspective of realizing the economic efficiencies promised by closer-to-perfect competition in the former.

A wholesale pricing regulation regime could be narrowly tailored to achieve such a goal. One would, of course, have to remain wary of association between arms-length affiliates. These potential pitfalls are well known to the Commission and have been for some time. (See: CRTC 87-13)

Wireless networks are definitely NOT natural monopolies. There is no question they are extremely expensive to build and maintain but let’s not forget that WSPs compete on multiple fronts – network coverage, network quality, customer service, handset selection, distribution channels, features, price, etc. If you start normalizing/equalizing any of those competitive attributes you are actually decreasing the competitive landscape rather than increasing it.

Petrochemical refineries and automobile manufacturing plants are also extremely expensive to build and operate but that doesn’t mean they are natural monopolies or candidates for structural separation of the production and retail operations of the business.

I think we have seen more than enough failed attempts over the years by the CRTC to create “new competition” through competitive access and wholesale tariffs to know that doesn’t really work. At the end of the day someone still has to invest in the network infrastructure and ongoing technology upgrades.

Mike:

1. The forms of competition you mention are subordinate to competition amongst investors for ROI, which I think you tacitly concede in your final paragraph.

2. Funny you should bring up gas and cars. Both of these industries already feature a separation between production and distribution. In the latter, manufacturers are by law not allowed to own dealerships.

3. More competition (in the form of new market entry in facilities-based service provision) from investors is clearly not forthcoming. So we should just throw our hands up, and the CRTC should just give up on its legislated policy objectives?

Your last conclusion seems to be little more than ideological flag waving. What we need is people thinking about creative solutions.

Ben

Creative solutions, really? What problem are we trying to fix? The latest CRTC report shows that average wireless prices in Canada are 40% cheaper than the US and more or less in the middle relative to other jurisdictions with comparable advanced economies. And those other jurisdictions generally have significantly inferior networks. Is there truly a cost-of-service problem that needs to be addressed?

The EU is living proof that the Conservative goal of 4 wireless carriers (or more) will lead to massive reductions in investment and erosion in the speed/quality of networks. I’m not sure that is a goal we should set our sights on as a country.

It was interesting to watch the vast majority of media editorial boards across the country come to the same conclusion this past summer – the actual problem the PMO is trying to fix is being perceived as a consumer champion to help get re-elected.

Regardless of what any of us think, the big wireless companies have already figured out that three capable carriers is the maximum any market can sustain and they’re not willing to expose their capital to that much risk. You are already living the reality of an overcrowded carrier market in Manitoba – no one willing to put much more capital at risk. The additional risk of adhoc, inconsistent and unpredictable regulation of the industry only serves to scare off potential new competitors. And, enticing potential competitors with financial or structural favors only creates companies that are forever dependent on “government regulated welfare”

I don’t see that there is a real problem that needs fixing and the CRTC’s latest report supports my conclusion.