Perhaps more than ever before, the availability of universal on-line connectivity has been a prominent part of the public conversation. With people stuck at home, awareness of the digital divide has never been more profound.

It is worthwhile taking a look at intermediate successes that should be celebrated. We should take the time to understand the significance of factors that lead to success, to see if we can replicate them in other areas.

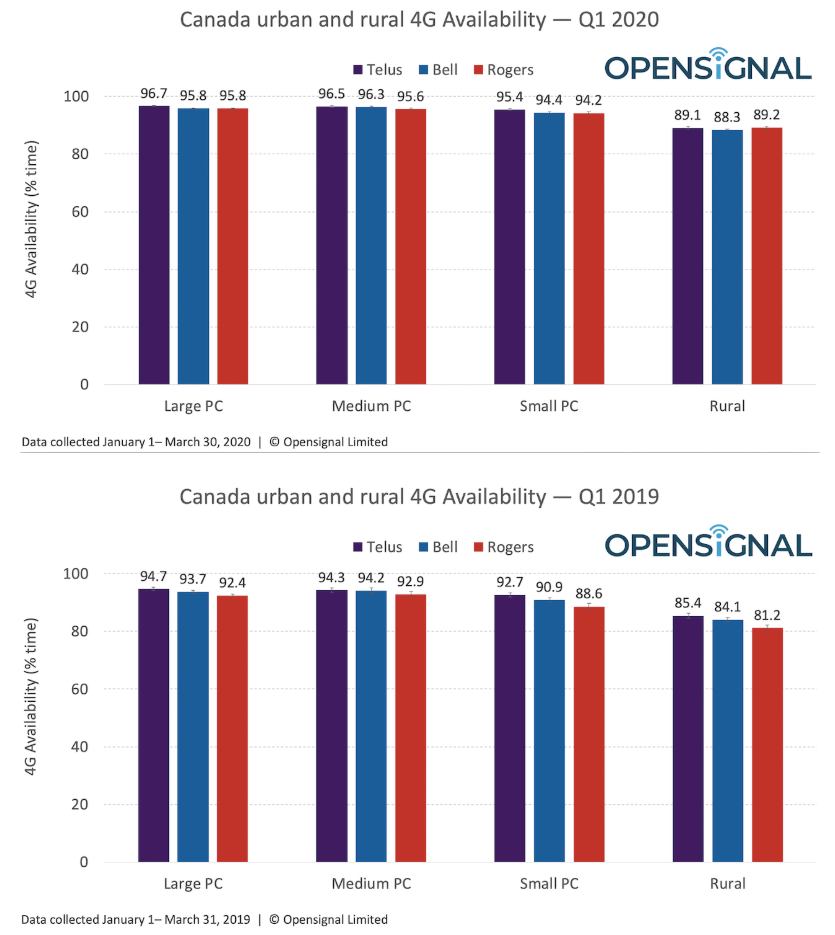

Canadian carriers’ investment in mobile wireless has resulted in Opensignal declaring last month that Canada has the world’s fastest mobile networks. A follow-up Opensignal report tells us that “rural users in Canada on the networks of Telus, Bell Mobility and Rogers have download speeds that surpass those experienced by users in most countries.” Indeed, the report continues, saying “rural Canadian users have far better download speeds than users in five of the seven G7 countries in the world.”

While there is more work to be done in 4G availability in rural markets, Opensignal indicated that rural 4G access climbed to nearly 90%, up to 10% higher than last year.

Canada’s policy framework favouring facilities-based competition in mobile services has delivered world leading network quality, in urban and rural markets.

How do we make sure that all Canadians have access to reliable, high-speed fixed communications, including voice and high speed internet?

How should the various levels of government create the right policy environment, policies, stimulus and incentives to accelerate investment programs in un-served and under-served markets?

Still, at the end of the day, it takes more than technology to get everyone online. Universal adoption needs universal access and universal demand. Most government programs have targeted the denominator side of the equation, without sufficient focus on the numerator.

It just takes money to stimulate supply. And that over-sized ceremonial cheque makes for a great photo op.

Stimulating demand is a lot harder.

We need to start working harder at doing that hard stuff.

Statistics Canada data shows that household computer ownership has stagnated at 84-85% since around 2013. Indeed there are apparently more households that have internet service than those with computers.

Do we understand why?

What steps will we take to address the needs of Canadians who have access to affordable services, but still have chosen not to adopt digital connectivity.

As I have written before, “A national broadband strategy needs leadership to understand and deal with concerns and fears that may inhibit adoption. It will take more than technology to get everyone online.”

After watching the Federal Government’s Parliamentary Standing Committee on Industry, Science and Technology (INDU) May 7 meeting, Greg O’Brien wrote a commentary entitled “Federal committee nothing but bluster”.

“There’s a waste of two hours,” he wrote. “Not just my own time. Everyone’s.” Later on, Greg writes “You’d think they would want to get to the point, let witnesses speak, maximize their time with a number of good questions. Nope. Maximum windbaggery is what I saw”.

I’m certain we both had higher hopes for last Thursday’s (May 14) meeting, when representatives from Rogers, TELUS, Cogeco and Xplornet were witnesses. I came away shaking my head.

While some productive discussion emerged, too much time was spent by Parliamentarians apparently building transcript materials to show off to constituents and future voters. As stated by Chair Sherry Romanado (MP – Longueuil—Charles-LeMoyne) at the beginning of the video record on “ParlVu”, the meetings are being held “for the purpose of receiving evidence concerning matters related to the government’s response to the COVID-19 pandemic.” Starting on April 23, there have been 7 such video conference meetings so far.

The meetings have evolved to become a forum for issues related to accelerating the deployment of broadband access in rural and remote parts of Canada. This has given rise to Michelle Rempel Garner’s May 7 release of the ‘not ready for prime time’ Conservative caucus “Connect Canada” plan, and NDP MP Brian Masse’s release of the “NDP Plan for High Speed Broadband Internet for all Canadians” just prior to the May 14 Committee meeting.

The opposition parties created their plans prior to hearing from witnesses, many of which are in the business of building and operating networks. That is disappointing enough. But Canadians should watch the performance of their parliamentarians in committee. How many would approve of a methodology that sees plans developed and conclusions drawn well in advance of gathering evidence?

For example, the opening remarks by Rogers for Business President Dean Prevost included this testimony that could have provided guidance for the plans [17:30:25]: “Unfortunately, where we do not have high capacity, high speed wireline networks, we are not able to provide unlimited wireless data for internet access at home at this time. Put simply, wireline networks have 50-200 times the capacity per consumer as rural wireless mobile networks. Removing datacaps would simply overwhelm the mobile wireless network, impairing service for everyone in that area, including the first responders and 9-1-1 services that rely on it.”

During last Thursday’s meeting, I was particularly disturbed by a couple exchanges between Calgary-Nose Hill MP Michelle Rempel Garner (‘MRG’) and TELUS Chief Customer Officer Tony Geheran (‘TG’).

We witnessed this exchange at 6:31 pm:

MRG: “Mr. Geheran, I think I am saying your name right. You made a comment tonight. You said ‘if you have a policy that fundamentally undermines an investment strategy, you have to change policy’ and I think I agree with that. So I’d start with saying, do you think that structurally separating the builders of network from Internet Service Providers is a way to solve the policy tension that I just described?”

TG: “No, I don’t. I haven’t seen that work anywhere globally, to sustainable effect.”

MRG: “It’s in the UK, right?”

TG: “Yeah.”

MRG: “It’s like the primary model in the UK.”

TG: “But if you look at the UK, they are wholesale moaning about the quality of their infrastructure, their lack of fibre coverage. across what is a very small geography. I know. I originated from there. And quite frankly, the Canadian networks are far superior in coverage and quality and performance through COVID has demonstrated that.”

MRG: “Well, that’s certainly not what we’re hearing in our offices from end users and that’s not the reality that we’re hearing in testimony tonight from you.”

I’m not sure the Honourable Member actually heard contradicting testimony that night. Perhaps she was confusing meetings.

So, I went off to find some independent sources to figure out what is actually going on in the UK. If the Committee members want independent corroborating evidence for Mr. Geheran’s perspective, they too can check with the independent regulators in Canada (the CRTC) and the UK (Ofcom). It didn’t take much effort to find information on the respective regulators’ websites.

Just a few weeks ago, in its April 24 Notice of Consultation reviewing its approach for rates for wholesale telecom services, the CRTC wrote “Ofcom has identified the lack of incentives to invest in new broadband networks, including full-fibre networks, as one of the key challenges facing the U.K. telecommunications industry.” Just 3 weeks ago, Canada’s regulator stated that the one of the key challenges facing the UK regulator was its lack of incentives to invest, just as Mr. Geheran had told Ms. Rempel Garner.

For verification of quality differences, there is plenty of data in the most recent annual reports from both regulators. For example, Ofcom is showing that broadband speeds in the UK increased 18% between 2017 and 2018 to reach 54.2 Mbps. According to the CRTC, average speeds in Canada reached 126.0 Mbps by the end of 2018, an 89% increase over 2017.

Or, the members of the committee could take a look at the Insights section from Ookla speed test results, which show Canada’s April 2020 wireline average at 118.11 Mbps for downloads and upload average at 51.80 Mbps. In the same period, wireline users in the UK were getting roughly half the download speed at 67.23 Mbps and about a third of the upload speed (18.28 Mbps).

When the Hon. Member from Calgary Nosehill said “that’s certainly not what we’re hearing in our offices from end users and that’s not the reality that we’re hearing in testimony,” the independent evidence supports ‘the reality’ portrayed by Mr. Geheran.

If they are hearing otherwise, the committee might want to take more time listening to different witnesses. Recall the opening of the meeting, where we hear that this inquiry was “for the purpose of receiving evidence”.

How would you interpret “receiving evidence”? Listening? Probing? Researching? Learning?

Instead, what we, the Canadian voters, have witnessed so far appeared to be parliamentary puffery.

At some point, we’re going to emerge from isolation and begin the normalization process for our lives and livelihoods.

When will that be?

When can that be? What kinds of key indicators will let us know that it is safe to relax certain restrictions?

What kinds of principles should guide us in understanding how to manage risks of viral transmissions? How (and when) do we begin to have government and industry collaborate to develop workplace standards and protocols to mitigate transmission risks?

Last Friday, the Crisis Working Group of the C.D. Howe Institute released an important report, “Canada Needs “Playbook” For Restarting Economy” [pdf, 167KB]. The Institute’s Working Group on Business Continuity and Trade (co-chaired by former Ontario Minister of Finance Dwight Duncan, and GE Canada VP Government Affairs and Policy Jeanette Patell) “discussed the need for a “playbook” to restart Canada’s economy, the implementation of supports for businesses to “bridge” the present shutdown, and the importance of continued investment in robust telecommunications infrastructure to meet the current surge in demand.”

While the focus of the discussion was an examination of the general economy, nearly a quarter of the report is dedicated to the telecommunications sector, recognizing “the important enabling role of Canada’s resilient telecommunications services during this crisis.”

The working group acknowledged the challenges facing telecommunications providers to maintain network reliability amid record usage levels when “every day is Superbowl Sunday.” Looking ahead, the roll-out of next generation networks will be essential for helping Canadians to adjust in a “new normal” (e.g., sustained “work from home”) for Canada’s economy post-crisis.

…

Members particularly emphasized that Canada’s telecommunications services have sustained economic activity as many Canadians switch to working by remote connection at home. The resilience of telecommunications networks today is a result of past investments and current efforts in the field to maintain infrastructure. Network providers are also rapidly building new facilities where these are needed – for example, to service remote learning for students and temporary medical facilities.

The report contains suggestions for measures governments could undertake to encourage further network resilience post-crisis, by providing incentives to accelerating capital investment by service providers. Referencing an report from a month ago [discussed in my blog post: “Could political interference create ‘sovereign risk’ for Canada’s digital infrastructure?”], the working group observed “government policies directed at reducing prices for telecommunications services (such as low rates for mandated access by resellers to telecommunications facilities) may discourage future investment.”

Looking ahead, the roll-out of next generation networks will likely be necessary in a “new normal” for Canada’s economy post-crisis. “Work from home” is likely to be sustained until the COVID-19 virus is fully contained. Fast and reliable telecommunications services will be essential for helping Canadians to adjust.

Recall, the group had previously stated, “If government pursues short-run political objectives at the expense of returns on long-lived infrastructure investments, certain Council members believe confidence in Canada’s regulatory regime for telecommunications will be difficult to win back.”

As a recent Intelligence Memo observed, “Recent experience demonstrates that, whatever discontents the federal government may be channeling, the quality and coverage of Canada’s networks, the cost of services, and the variety of platforms and carriers available, is impressive. Our telecommunications infrastructure is a vital asset. Good public policy should strengthen it.”

A new report released this morning warns “Mandated access could impair Canada’s next generation of digital infrastructure.” The report, “Mandated Competition or Free Ride?” [pdf, 329KB], expresses “concern” that the CRTC would act on political directions to reduce wireless prices and warns of the potential impact of the Minister’s mandate letter on the perception of independence of Canadian regulatory institutions.

In the context of the CRTC’s recent Wireless Review proceeding, as well as the ongoing Cabinet appeal of last year’s wholesale broadband decision [Telecom Order CRTC 2019-288], the Competition Policy Council of the CD Howe Institute held an ”ad hoc” meeting in February to discuss the issue of mandating access to telecommunications facilities. Members of the Council highlighted a lack of clarity for what consumer price level the federal government views as “economically efficient”. The report says certain members of the Council “doubted that the federal government has an empirical basis for its [25%] price reduction target. These members believed that the federal government has established its target arbitrarily and for political aims.”

The report notes the significant risk of setting wholesale rates ‘wrong’ and says that most members of the Council were “skeptical of the institutional competence of the CRTC to consistently identify the ‘right’ regulated rates for mandating access.”

The consensus of Council members present was that competition in telecommunications services involves fast-paced technological change, long lead-time investment in facilities, multiple and highly differentiated service offerings, consumer demand for high-quality services, and rapidly evolving cost structures. All Council members were cognizant of the “enabling” impact of high-quality infrastructure for digital services on Canada’s overall competitiveness. While certain Council members contended that mandated access would provide downward pressure on consumer prices, other members were concerned that short-run price reductions would come at the expense of long-term investment incentives for next-generation facilities. Council members agreed that setting rates for access at too low a level below facilities providers’ required return on infrastructure investments would discourage future investments.

Members of the Competition Policy Council said “Setting rates for access at too low a level below facilities providers’ required return on infrastructure investments would discourage future investments.”

Council members agreed that facilities to transmit information – whether by signals over wireline infrastructure or using radio spectrum – are essential for providing communications services. The question at the core of the discussion was whether competitors ought to build their own facilities, or whether mandating access by some competitors to other competitors’ facilities is preferable.

Recording the divergent views of some members of the Council, the report takes on the tone of ‘meeting minutes’ of the debate among council members:

One group of Council members argued that the CRTC should increase mandated access – particularly by allowing MVNO access to wireless transmission facilities at regulated wholesale rates. These members contended that the CRTC should not assume that the only way to compete is to build alternative transmission systems and operate them more efficiently. In these members’ opinion, such “facilities-based competition” is an out-dated concept in the current technological setting, in which they contend great efficiencies can be generated by superior computer power and algorithms without the need of owning and running hardware transmission facilities. While acknowledging that mandated access requires close attention to appropriate access prices, this group of Council members contended that facilities-based providers would continue to have an efficient incentive for new infrastructure if the CRTC adopts a “cost plus” framework for setting rates for mandated access. That is, these members argue that rates can be calibrated to provide sufficiently high risk-adjusted returns on capital to preserve incentive for new investment at the margin.

In contrast, as discussed further below, a second group of Council members expressed scepticism that the CRTC would have the capacity to set appropriate prices for access that provide the appropriate risk-adjusted rate of return to investment in facilities.

These sceptical members contended that mandating access has failed empirically to foster durable competition. For example, certain members pointed to the CRTC’s arguably unsuccessful earlier approach to compelling unbundling of local loops for telephones in order to foster competition in voice services. Nonetheless it was the development of voice services provided through cable and fiberoptic facilities (e.g., VoIP) that ultimately produced new competitors for telephone facilities.

In this way, these members observed that regulators tend to be “backwards-looking.” That is, regulators arguably focus on static sources of competition. By assuming that existing infrastructure will be the only technology for delivering a given service, certain Council members believe that regulators run the risk of interfering in the dynamic that drives entry of durable new facilities-based competition.

The report concludes with a discussion warning of political interference in the independence of Canada’s telecommunications regulator. “If government pursues short-run political objectives at the expense of returns on long-lived infrastructure investments, certain Council members believe confidence in Canada’s regulatory regime for telecommunications will be difficult to win back.”

According to members of the Council, politically driven policy shifts that result in reduced returns on past investments will be viewed by the investment community as a form of sovereign risk “unless political decision-makers make credible commitments to an independent regulatory process grounded in consistent principles.”

With the COVID-19 pandemic leading more Canadians to work from home, some people are asking if this will put too much stress on the networks or on consumer service plans.

The good news is that Canada’s networks are ready for working from home, even with kids streaming videos while home for March break or closed schools, and very few types of work should put undue strain on typical residential subscriptions.

Bandwidth requirements for video-chat applications

Zoom

Screens

Up

Down

Single Screen

2.0 Mbps

2.0 Mbps

Dual Screen

2.0 Mbps

4.0 Mbps

Triple Screen

2.0 Mbps

6.0 Mbps

Screen Sharing Only

150-300 kbps

150-300 kbps

Audio Only

60-80 kbps

60-80 kbps

Google Hangouts

Use

Up

Down

Minimum Requirements

300 kbps

300 kbps

Two-person Video Calls

3.2 Mbps

2.6 Mbps

Group Video Calls

3.2 Mbps

3.2-4.0 Mbps

Skype

Type of Call

Up

Down

Voice Call

100 kbps

200 kbps

Video Call (2 participants)

600 kbps

600 kbps

Video Call (3 participants)

600 kbps

2.0 Mbps

Video Call (5+ participants)

600 kbps

4.0 Mbps

Contrast these relatively low speed requirements to Netflix, which Popular Science says needs 25 Mbps for its highest quality content, or 3 Mbps for its standard definition streams.

We know that the greatest consumption of residential internet bandwidth is high definition streaming video. Very few work-at-home applications would come close; hardly any would involve sustained levels of streaming data that rival delivery of 4K video streams.

According to the CRTC’s Communications Monitoring Report, in 2018 (almost a year and a half ago), more than half of Canadian home had already subscribed to residential internet packages with more than 50 Mbps download speeds. The average residential download speed in 2018 was 126 Mbps, double the speeds experienced in the United States. A third of Canadian households subscribed to speeds faster than 100 Mbps.

According to the CRTC, “The average amount of data downloaded by residential Internet service subscribers increased by 25.4% between 2017 and 2018 to 192.9 GB per month, and by an average of 30.5% annually from 2014 to 2018.”

As temperatures begin to reflect the annual Spring thaw, it marks the beginning of outside plant construction season for wireline and wireless carriers in Canada seeking to invest in capacity upgrades and service expansion to underserved regions.

As government prepares an economic stimulus plan, I can't help thinking of various recent regulatory and policy actions that created disincentives for investment in the telecom sector.

Billions of dollars in broadband and mobile network upgrades and expansion.#crtc#cdnpoli

Perhaps more than ever before, the availability of universal on-line connectivity has been a prominent part of the public conversation. With people stuck at home, awareness of the digital divide has never been more profound.

Perhaps more than ever before, the availability of universal on-line connectivity has been a prominent part of the public conversation. With people stuck at home, awareness of the digital divide has never been more profound.