I found it fascinating to see that only 2 of the top 5 posts were written this year. The archives continue to provide interest to so many readers.

Which of my blog posts resonated the most with you? I just posted my year-end wrap-up yesterday, so it hasn’t had a chance to crack the Top 5… yet!

Thank you for following me here on this blog and on Twitter [X], and thank you for engaging online and by phone over the past year.

Click here to subscribe to my weekly email newsletter, with its digest of the previous week’s blog posts.

I hope the coming holiday period provides an opportunity to connect (in person) with your family and friends. I will be back in the New Year. In the meantime, let me repeat my very best wishes for health, happiness and peace in the year ahead.

Somedays, more than others, I really do feel the years spin by.

As I wrote last year, I am continuing to use lyrics from Joni Mitchell’s Circle Game as the title of my year-end wrap-up.

So the years spin by and now the boy is 20

Though his dreams have lost some grandeur coming true

There’ll be new dreams, maybe better dreams and plenty

Before the last revolving year is through

No question. The years seem to be spinning by ever so quickly, but I’m not ready for that “last revolving year”… yet. There is so much still that needs to get done. So much that I wrote about last year remains just as valid today.

Improved access to quality information is the presumptive raison d’être for Canada’s Online News Act, Bill C-18. While I understand the motivation behind the legislation, as I have written, its implementation was badly fumbled.

Unfortunately, I am concerned that this is another case of government focus on the supply side without consideration of factors impacting demand. With all the best funding in the world to create better news, are we doing enough work to ensure there is a market to consume that news? Just as I have frequently complained about our work on broadband, we seem to be better at stimulating supply, and rely upon a Field of Dreams hope for the demand side. What if you build it and they don’t come? There are a number of ways to improve funding for news, but how does that help deliver quality information to a generation who don’t watch linear TV, and don’t pick up a newspaper, or rely upon news websites?

What do we do if we provide funding to create high quality local and national newsrooms, but a generation of consumers rely on 30-second high-energy video clips where adherence to facts isn’t valued as highly as the entertainment quality by the search algorithms?

Will digital literacy training in elementary and secondary schools include teaching how to differentiate between information, misinformation, and disinformation? How can we create more sophisticated consumers of high quality content?

Dealing with supply side issues is relatively easy. In most cases, if you throw enough money at the problem, it gets solved. Whether it is building broadband, funding newsrooms, creating quality Canadian media content, supply can be stimulated with injections of cash. Dealing with the demand side is much more challenging. What do we do when Canada’s universal broadband objectives are met, but more than a million people remain off-line? The issue of driving increased adoption will need to be a carry-over from my 2023 agenda into next year.

Last week’s “Checking my scorecard” provided more reasons for why I think it is too early to consider hanging up the ol’ keyboard.

Looking at what I set out as my 2024 agenda, I see that we made progress on some items, but others, such as the issue of driving increased adoption, will need to be carried over once again. I continue to shake my head, in both amazement and dismay at academics who think the best solution to all broadband afflictions, both adoption and rural access, is building municipal or government-owned fibre.

I added 72 blog posts to “Telecom Trends” over the course of 2024, continuing to write 1 or 2 posts per week. There are now more than 3325 posts in the archives (fully searchable). I continue to send out my weekly newsletter; you can subscribe here.

As I have said in the past, it is my objective for this blog to be a source of quality information on Canadian telecom policy, with occasional gastronomical diversions. The past year has seen me add content dealing with the rising levels of antisemitism and online hate in this country. This content rightfully belong on a blog looking at Telecom Trends because of the tie-in to proposed Online Harms Legislation.

I look forward to engaging with you in the New Year, as the years spin by toward another spring and summer.

I wish you and your families a happy, healthy, safe and peaceful holiday season.

Universal broadband adoption is turning out to be one of those “evergreeen” items. There are two sides: supply; and, demand. Most activity focuses on the supply side, ensuring the availability of broadband wherever people are, at home or on the road. Solving the supply problem is relatively easy. It reduces to an engineering and project management problem. Given sufficient financial, human and technology resources, we know how to deliver broadband. Demand is a tougher problem. It isn’t a matter of building it and everyone will join the party. Driving universal broadband demand means understanding all of the factors that contribute to resistance to get online. Stimulating the demand side of the adoption equation requires developing an understanding of the human factors resisting getting online, factors that don’t necessarily correspond to logic. This ties to the Digital Literacy bullet on the agenda as well.

Online harms

Canada’s Online Harms Act has been introduced, but it is stalled at second reading and has not yet been sent for committee study. It is at risk of dying on the Order Paper due to the Conservative filibuster over the $400M Sustainable Development Technology Canada scandal.

Regulatory overreach

I recently wrote about regulatory overreach because of the abusive process being used by the CRTC to pressure service providers. I also expressed concerns about elements of the CRTC’s strategic plan. The Commission is unable to release decisions in a timely way to the point that it will have to relax its grip on the industry.

However, as discussed in the next section, the CRTC is hardly an “independent” regulatory body, with so much of its workload being determined by Parliamentary actions and Ministerial references. Government is just as much to blame. I find it ridiculous that a Private Member’s Bill was able to amend the Telecom Act to have a permanent reference to last week’s CRTC public notice on internet nutrition labels. From the First Reading in June 2022, through Royal Assent in late June of this year, no one had the courage to publicly state that this didn’t need legislation.

Telecommunications is a sector that requires billions of dollars in annual investment – investment that abhors regulatory uncertainty. At some point, we need greater push back from the CRTC, and more knowledgeable parliamentarians and policy advisors, or we will continue to be mired in delays driven by consultative processes.

Mandated wholesale access

A post by my colleague Ted Woodhead displays optimism about improved balance in the CRTC’s interim wholesale fibre rates decision, released October 25. We’ll continue to watch that file. But shortly after that decision was released, on November 6, Cabinet sent an earlier wholesale fibre decision back to the Commission for “review”. How will the final rates impact investment? As I asked in my post “Tangled up in red”, didn’t the CRTC’s October rates order explicitly address the issues raised by the Cabinet reconsideration directive?

A few weeks ago, the CRTC announced the launch of 3 consultations “on making it easier for Canadians to choose the best Internet and cellphone plans”. CRTC 2024-293 (Enhancing customer notification), CRTC 2024-294 (Removing barriers to switching plans), and CRTC 2024-295 (Enhancing self service mechanisms) all have deadlines for submissions of January 9, 2025 with replies due January 24. For me, the risk of customer confusion arising from self-service mechanisms creates my greatest concern.

These consultations arose from a Parliamentary direction, in this case, changes to the Telecom Act introduced as part of the Budget Implementation Act. The Telecom Act changes were just two pages out of the 686 page Act, which provides a clue as to the depth of review (or lack thereof) that was applied to the legislation.

Keep in mind, the CRTC’s Wireless Code has been around since 2013, and modified in 2017. The Internet Code has been in force for nearly 5 years. These Codes were created following extensive consultations. Will the CRTC be able to find effective ways to work around the government’s naively constructed amendments to the legislation, using a short 6-week process?

That same week, there was a fourth notice of consultation in response to political activity as the CRTC sought comments on the Cabinet instruction to reconsider the Commission’s wholesale fibre decision. For years, telecom policy reviews have called for less political interference in the workings of the CRTC. Indeed, the objectives set out in the Telecom Act call for “increased reliance on market forces for the provision of telecommunications services and to ensure that regulation, where required, is efficient and effective”. This will be a subject worth examining in greater detail, especially as we head into an election in the coming year.

Impacts of investment on coverage and resilience

Checking my scorecard, I am reminded that I wrote about how easy it can be for regulators and policy makers to lose focus, to lose sight of the prize. The CRTC had just released its “Competition in Canada’s Internet service markets” decision which opens saying “The Commission is taking action to ensure that Canadians benefit from affordable access to high-quality Internet services.” The CRTC said the right things in that regulatory policy decision:

In setting out its regulatory framework, the Commission seeks to create opportunities for innovative competitors to differentiate themselves and bring new choices to consumers. Importantly, this is not the same as guaranteeing that one type of competitor can profitably compete without risk. In respect of wholesale HSA services, the Commission enables wholesale access at just and reasonable, cost-based rates. It is then up to competitors to find commercial strategies that deliver an attractive value proposition that responds to consumers’ needs.

As I wrote, we often lose sight of the prize. The wholesale framework is a means to an end, not an end in and of itself. It isn’t the role of the regulator to preserve the independent wholesale-based competitive ISP industry. We don’t guarantee “one type of competitor can profitably compete without risk.” This theme – and its impact on investment – is certain to continue playing a prominent role next year.

Digital literacy

Two weeks ago, I discussed the new analysis of Statistics Canada data on technology adoption. That report says “targeted solutions, including measures to improve digital literacy and skills, especially among older adults, would appear to be more logical and efficient than broader, more disruptive, industry structural changes.” Targeted measures to improve digital literacy and skills would require investment in training – an investment in people. Such investments are much harder work than building broadband access. Investing in digital literacy doesn’t create the same kind of photo op as an investment in infrastructure, but it is just as important. This item will once again be carried forward.

Looking ahead

Checking my scorecard from last year helps me prepare an agenda for 2025. What else would you like to see added to the Canadian telecom policy agenda?

A few weeks ago, Bell released a new report, Navigating the Generative AI and Cybersecurity Journey [pdf, 580KB]. The study, prepared with Maru Research, surveyed a diverse group of 600 business leaders, information technology (IT) and security professionals from medium and large-scale enterprises representing a wide cross-section of industries.

The report looks at how organizations have adopted Generative AI (GenAI) in their workplaces, as well as where the technology has been found to be most beneficial.

Among the highlighted findings:

About 60% of Canadian organizations that have adopted AI, have limited to no AI strategy in place to guide deployment, risks and expected value.

Reducing and automating tasks is the top GenAI use case amongst Canadian businesses, followed by drafting and editing documents.

Improved quality of product (54%) and a decreased time to market (52%) have been cited as key return on investment areas for early GenAI adopters.

Bell found 71% of professionals at medium to large enterprises are using GenAI to some degree; and, 41% are using it on a regular basis, with tools like ChatGPT making the use of AI especially accessible.

While GenAI is revolutionizing workplaces, organizations are being prudent about the risks. Among early adopters, the study heard about cybersecurity concerns. A third of the organizations are anxious about bad actors tampering with their AI systems; a quarter worry about theft of sensitive data; and, about 10% expressed concern about bad actors manipulating inputs into their systems.

IT and security professionals were found to be focused on proactively mitigating the security, legal and reputational risks that GenAI may present before fully adopting. About three quarters said that concerns about potential risks slowed the adoption of GenAI fairly significantly, while other organizations have moved ahead by implementing safeguards.

While some industries are still exploring the best use for GenAI, retail was found to be leading in adopting the technology for production use, including customer-facing applications and inventory management.

There is optimism reflected in the report.

Despite the challenges, many Canadian organizations are optimistic about the future of AI – almost half expect we are just at the beginning of AI model progress and much more progress will take place over the next five years. Looking at how AI adoption influences this sentiment, early adopters expect moderate advancements over the next five years, while mainstream businesses anticipate even more significant breakthroughs. The consensus is clear: generative AI is just getting started and its role in reshaping Canadian industries will continue to expand.

My key take-aways from the report? The best outcomes for adopting GenAI in the workplace will be achieved by organizations placing a priority on governance, deploying multi-dimensional approaches to security risks, and improving threat detection using AI to manage those risks.

Communic@tions Management Inc. (CMI) published “Technology adoption, use, and affordability in Canada” [pdf, 1.1 MB], documenting key indicators for how Canadians relate to the internet and smartphones. Through the years, CMI has developed an expertise in analyzing and interpreting Statistics Canada publications, in addition to developing custom tabulations and correlations of the raw Statistics Canada data.

CMI estimates that in 2023, 95% of Canadian households had home internet connections, and 90% of households had smartphones. An additional 5% of households had mobile devices that were not smartphones, for total mobile adoption rate of 95%.

CMI notes that in 2021, more than half of Canadian households now rely exclusively on cell phones for their phone service – a notable milestone.

CMI took a look at spending by income quintile (similar to what I have done in the past) and added in a comparison to spending by income quintile in the US. “Across most income groups, Canadian households spend less on cellular service than do Americans.”

While we know that the mobile phone has become a substitute for wireline phone service, CMI says “it is not unreasonable to state that the smartphone has substitution effects for landlines, photographic services, newspapers, and magazines and periodicals.” Looking at other data from the 2021 Survey on Household Spending, CMI found the following changes in average household spending on each of these items from 2010 to 2021:

Landline telephone services -56.4%

Photographic services -42.8%

Newspapers -27.3%

Magazines and periodicals -50.0%

During that period, the number and percentage of households with cell phones was increasing – from 78.1% of households in 2010 to 93.9% in 2021. And, within those totals, an increasing number of devices were smartphones.

CMI also notes that the Survey of Household Spending estimated there were 13,297,000 households, of which 10,378,000 had cell phones. Using Statistics Canada data, CMI estimated there were at least 17,772,000 cell phones in use at that time. By 2021, 14,197,000 out of Canada’s 15,123,000 households had at least 26,759,000 mobile phones. “In other words, from 2010 to 2021, the number of total households went up 13.7 per cent; the number of households with cell phones went up 36.8 per cent; and the number of cell phones in those households went up 50.6 per cent.”

Using data from custom tabulations of Statistics Canada’s General Social Survey, CMI found that smartphone owners were almost twice as likely to read news online daily, compared to those that do not own smartphones; and smartphone owners were less than half as likely to read a print copy of a newspaper daily, compared to those that do not own smartphones.

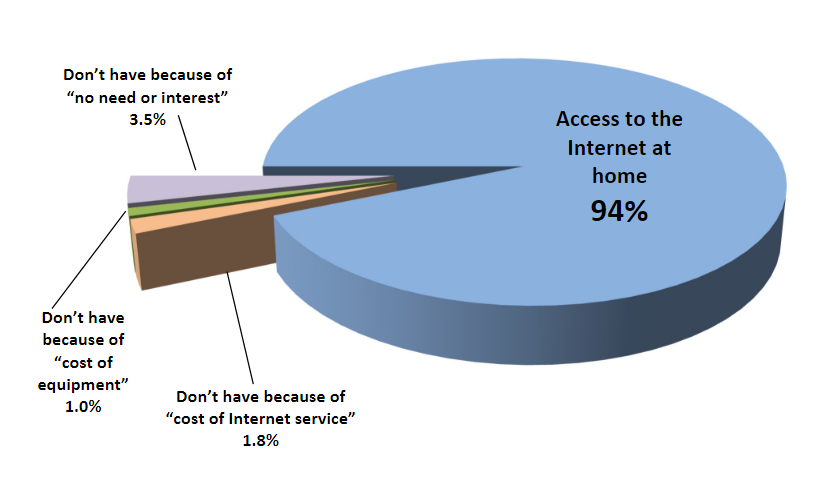

To examine affordability, CMI turned to Statistics Canada’s 2022 Canadian Internet Use Survey (CIUS). As seen in the figure, “home Internet is nearly ubiquitous for Canadians, and “no need or interest” is the most important reason for non-adoption.”

Adoption varies by age, ranging from 99.3% in the age group 15-24; 98.8% for ages 25-34; 98.0% for ages 35-44; 96.7% for ages 45-54; 93.1% for ages 55-64 and 83.7% for those 65 and older. In each segment, “No need or no interest” was the dominant reason for non-adoption, beating out “the cost of equipment” and “the cost of the service”. CMI stated “In other words, there is much more likely a demographic link based on age than an affordability link based on income.” Similar results were found for smartphone adoption.

There are clear policy implications that arise from CMI’s work. As CMI says,

Thus, one might say that the adoption of Internet and smartphone technology in Canada is nearly ubiquitous, with age and attitudes a much greater factor than affordability when influencing non-adoption.

To the extent it is a goal of public policy to maximize adoption – and use – of these technologies, targeted solutions, including measures to improve digital literacy and skills, especially among older adults, would appear to be more logical and efficient than broader, more disruptive, industry structural changes.

It is worth emphasizing that sentence: “Targeted solutions, including measures to improve digital literacy and skills, especially among older adults, would appear to be more logical and efficient than broader, more disruptive, industry structural changes.” This resonates with themes you have seen before on these pages.

The distillation of data in the report is worth keeping in mind as we turn our minds toward 2025 plans and objectives. Targeted solutions will be an approach for policy strategists to keep in mind when developing platforms for the 2025 election.