Are Canadian mobile prices higher than in other countries? Certainly. Are the prices too high? That cannot be answered without considering factors that contribute to higher costs for operators.

The article, by economists Mark Meitzen and Nick Crowley, was based on a study conducted for TELUS by Christensen Associates [pdf, 272KB].

The key conclusion of the study was that “Canadian wireless providers face significantly greater cost pressures than carriers in other countries on key network inputs and factors like climate and size of coverage area that impact costs. These cost pressures contribute to price disparities between Canada and other countries.”

Among factors examined in the study:

Capital expenditures: Canadian wireless network capital expenditures per subscriber are 50 percent higher than the Benchmark Country average.

Labour costs: Across all industries, Canadian companies face over 10 percent higher labor costs than Benchmark Countries.

Spectrum costs: Canadian spectrum prices are significantly higher than the average of the Benchmark Countries as well. In general, lower frequencies (the “coverage” band) provide extended coverage at lower cost as fewer base stations are required to achieve greater geographic coverage, whereas higher frequencies (the “capacity” band) are primarily used by mobile operators to cover urban and suburban areas where data traffic is dense and substantial network capacity is required. Canada has the most expensive spectrum among countries in the study. The capacity band is twice as expensive in Canada, while coverage spectrum is four times more expensive than the Benchmark Countries.

Operating environment: including geography, population density, and climate contribute to costs due to characteristics of the service provider’s service territory that are outside the control of the service provider but affect the magnitude of primary cost drivers described above.

As the authors conclude, “Simple comparisons of wireless prices across countries that fail to account for the cost differences in providing wireless service offer a distorted picture of the competitive landscape. This makes for bad economics and even worse public policy.”

Last week, I wrote about “Regulatory arbitrage” and tried to draw a parallel between “today’s proposed MVNOs and the long distance resellers of 30 years ago.”

A long time Canadian telecommunications regulatory colleague commented on that post and suggested that a better analogy might be local competition.

George Hariton wrote:

The parallel with long distance is interesting. But the more relevant analogy is the 1997 decision mandating incumbents to give new entrants access to their networks for local voice (POTS) competition. In particular, unbundled local loops are functionally similar to what some MVNOs are asking for (some MVNOs are asking for a lot more, of course). Back then, mandated access was justified by the “stepping-stone” or “ladder-of-investment” theories. In practice, local competition became a reality when cable companies used their own facilities to provide that competition, and when mobile services became enough of a substitute.

I guess we will have to learn that lesson all over again.

Let me point out that I don’t think anyone in the CRTC Wireless Review proceeding is saying MVNOs are evil and should be banned. The issue relates to whether MVNO access should be mandated, or if the decision should be left up to the operators (both virtual and facilities-based) to develop a mutually beneficial business case.

There is a long history that can provide guidance in telecommunications competition in Canada.

A few weeks ago, I wrote a piece called “How long is a piece of string?”, discussing the challenge of defining the price of a mobile service plan. Year over year comparisons are difficult because data usage increases so dramatically and service providers try to design new packages to meet the demand.

So, a question arose on how to measure achievement of a key element in the Minister’s new mandate, requiring him to “Use all available instruments, including the advancement of the 2019 Telecom Policy Directive, to reduce the average cost of cellular phone bills in Canada by 25 per cent.”

As it turns out, there was clarity to be found in the Liberal party’s platform, that set out 2 specific plans and promised a 25% savings within 2 years:

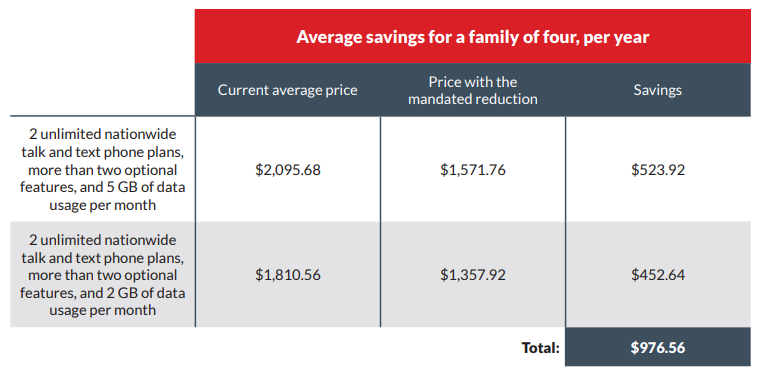

2 unlimited nationwide talk and text phone plans, more than two optional features, and 5 GB of data usage per month; and,

2 unlimited nationwide talk and text phone plans, more than two optional features, and 2 GB of data usage per month.

The platform priced these out and promised specific savings. The two plans with 5GB per month were said to cost $2,095.68 at the time, and the platform promised to reduce the bill to $1,571.76 for savings of $523.92 per year. The two plans with 2GB were said to cost $1,810.56, promised to drop to $1,357.92 for savings of $452.64. All told, this hypothetical family of 4 would have their annual $3900 phone bill drop by just under $1000 for a total of about $2930.

TELUS decided to test its plans and found that it now offers plans that already meet what it is calling a “True North Affordability” standard.

According to TELUS, the Platform scenario could be delivered with all 4 hypothetical customers each subscribing to TELUS 10 GB Peace of Mind plans, for a total of $2880. The family would save about $50 more than promised, and would receive 2 to 5 times the amount data specified in the Liberal party’s platform promise.

It is clear that Canada’s mobile marketplace has moved faster than anyone in Ottawa could have anticipated. But that doesn’t mean the goal posts should continually be moved.

At a time when service providers are beginning to make the massive capital investments associated with the next generation of technology, regulators and policy makers alike need to be concerned about the unintended consequences of intervening in the market. As the Competition Bureau noted in its conclusion to its November CRTC submission, “competition has not yet reached its full potential and a mandated MVNO policy applied broadly risks undermining the steps taken by wireless disruptors, without much certainty that the MVNO policy will significantly decrease pricing.”

The Competition Bureau is concerned that the regional mobile competitors, the “disruptors” that have acted as catalysts in the marketplace, will be disproportionately harmed by regulatory intervention.

As I wrote earlier this week, we should be talking more seriously about providing direct assistance to those disadvantaged households who really need help accessing affordable wireless technology and services.

Let me be very clear: Just because local prices may be higher than in other places, doesn’t mean a particular good or service is unaffordable at home. There are lots of things for which Canadians pay more than our peers to the south, or other countries. An awful lot of things. Some are basic needs, like milk, eggs and poultry. Some are everyday items like fuel or alcohol or electronics. We gripe about paying more, but the vast majority of us can afford to pay the price.

For most Canadians, mobile services are affordable.

There. I said it.

The affordability of mobile service is measurable. Every quarter, more Canadians are subscribing than ever before, meaning more Canadians are finding a mobile plan they feel they can afford. Quarterly financial results are showing increasing numbers of Canadians are upgrading their service plans, increasing their monthly bills because the new data packages deliver more affordable value. I know. It sounds like an oxymoron to say people are increasing their monthly spending because they are getting more value.

As I wrote a couple weeks ago, PwC recently produced a couple reports showing that “Canadian mobile services top G7 affordability ranking”. It is a headline that must have made many heads explode since it is completely contrary to the popular narrative. Looking at the data, PwC examined the affordability of wireless services for Canadians in proportion to income and compared that to other jurisdictions. In addition, PwC considered discretionary spending by Canadians, testing whether household budgets were being strained by spending on mobile plans. It turns out that household discretionary spending increased in every income quintile; at every level of income, year over year people had more money left over to spend on fun stuff, even after paying for their communications bills.

So, while we all might want our monthly bills to come down (and who wouldn’t want to pay less for everything we pay for?), the vast majority of Canadians are paying for mobile service that they felt they could afford when they signed up, and they continue to pay their bills each month.

And indeed, last week the CRTC released the results of its own survey and found that 83% of Canadians were satisfied with their current service provider, with 35% saying they are very satisfied.

So, can we please stop the empty rhetoric about “too much pressure” on the average Canadian’s household budget? It is distracting from the real question of affordability for that segment of Canadians who truly can’t afford a smart phone and can’t handle the price of a mobile voice and data plan. There is a real problem for a number of low income households. Their calls for help are getting lost amid the populist noise calling for across the board price reductions. Lowering prices or increasing data volumes for the same price doesn’t change the calculus for a household at the margins trying to choose between the luxury of President’s Choice macaroni and cheese or the yellow box No Frills version once again.

Those are the Canadians for whom we need to talk about affordability. That conversation just isn’t happening.

In the CRTC’s upcoming Review of Mobile Services, the Coalition for Cheaper Wireless Service has proposed that carriers be mandated to offer an income-tested mobile services plan with unlimited Canada-wide voice and texting, and 4GB per month of data at LTE speeds for $25-30 per month. The coalition was silent on the subject of how the low income household gets a hold of an affordable LTE compatible device. There is a lot of merit to a targeted affordability program. I am not crazy about having just one plan available for these households; I would prefer to see a portable direct subsidy for those who need the social assistance and allow them to select the best plan to meet their specific needs. It is also my view that no specific plan should be prescribed in a regulatory decision because of the potential for the market to make any plan obsolete.

Funding such a plan could be the subject of many more blog posts: should it be funded by a general tax on telecom revenues, like the Broadband Fund; or, perhaps it should be funded by social service government programs? By way of example, Ontario’s Electricity Support Program may be a useful model to examine.

In any case, we also need to work out a solution to get affordable devices into the hands of lower income households. That is a non-trivial challenge.

For many, we still need to show them the basics. There are too many who don’t see the value of a mobile broadband service at any price.

Our national digital strategies have to consider gaps in service adoption with the same focus as programs that target service availability. There are far more people who have access to service but haven’t subscribed, than there are people living in unserved territories.

Canada needs to talk more seriously about increasing adoption of digital technologies and services in lower income households. So far, there has been too much noise to hear about the real problems, let alone develop real solutions. We need to change that.

We need to talk seriously about affordable wireless.

Much of the media coverage has looked solely at the potential to mandate resale of mobile facilities via Mobile Virtual Network Operators – MVNOs. At least one reporter has mistakenly described it as a “hearing on Mobile Virtual Network Operators, wholesale service providers that offer services at cheaper rates”. In fact, no it isn’t, and no they aren’t.

There are other components to the CRTC review, including an important review of whether additional regulatory measures are required “to reduce barriers to the deployment of cellular infrastructure”, given that the next generation of mobile architectures imply “a large number of small cells will be required to properly cover any given area.” The public has not been as engaged in that topic, despite the potential impact on intergovernmental relations, electro-magnetic radiation concerns, issues associated with the visual impact of antennas on every lamp post among other matters. My views on such issues are already documented from my days in 2012-13 working on my local municipality’s tower siting protocols [for example, see “We need more towers” • Sept 2012].

But the question of mandating MVNOs is indeed on the agenda.

As I read through the business plans and follow the Twitter rhetoric, I just can’t get over the feeling that there is a parallel between many of today’s proposed MVNOs and the long distance resellers of 30 years ago.

Those businesses went through two distinct waves of failures.

The first wave was triggered by a dependency on regulatory arbitrage. The CRTC mandated wholesale inputs and the marketplace determined the maximum price that could be charged. Non-facilities based service providers relied on regulation to provide a sufficient margin to enable them to eke out a living.

The second wave was a failure to add value through innovation or differentiation. The product was the same as everyone else, just cheaper – and cheaper in every sense of the word. As retail prices fell, price savings became less meaningful and margins shrank. Resellers operating with regulated access became dependent on going back for rate reviews in order to maintain viability.

Some of those businesses survived; most have faded into oblivion.

What factors allowed a handful to survive?

Consolidation was a part of the answer, and diversifying into adjacent businesses is another part. Long distance, local phone service, home internet. Adding one business to the next, relying on regulated access to facilities based carriers’ lines.

Regulated rates for resale arbitrage has meant a continuous cycle of rate-setting procedings and shifts in technology has also driven more regulatory burden. If the regulator sets rates too high, there isn’t enough margin left for to arbitrage; if rates are too low, the facilities-based carrier has insufficient margin to expand its network coverage or invest in technology upgrades. It is a delicate balance, virtually impossible for the regulator to get “bang on”.

I can’t help feeling these companies are playing like the old video game Frogger, hopping to safety by jumping onto the next passing log. For some of the proposed MVNOs, mobile is apparently just a jump onto the next business adjacency, the next log coming down the stream to provide temporary safety to avoid drowning.

We’ve been down that river before.

I’d like to think there is a better way. I have some ideas for more forward-looking value-added services that don’t have such regulatory dependencies, looking ahead to the next generation of services, instead of arbitraged resale of yesterday’s success story.

Will any service innovations be discussed when the CRTC opens its hearing on Feb 18? Or are we setting up another round in the regulatory arbitrage game of Frogger?