A few weeks ago, I wrote about “Connecting the unconnected“, taking a look at various strategies to provide introductory connectivity to people who cannot otherwise afford devices or broadband service.

Some of these strategies involve providing access to a limited number of “zero-rated” services, such as Wikipedia.

Through the years, carriers have used (and continue to use) zero-rated offerings as a way to get people to expand their use of services. To this day, many companies have “social plans”, providing limited access to some social networking sites for a flat monthly rate.

Internet.org is a zero-rated service being offered in less developed countries seeking to provide affordable access to a limited number of sites. “Internet.org is a Facebook-led initiative bringing together technology leaders, nonprofits and local communities to connect the two thirds of the world that doesn’t have internet access.”

Like flat rate services in Canada, activists have criticized Internet.org for violating “net neutrality”, favoring Facebook over other websites and services.

In a news story this morning, BBC quotes Facebook’s founder, Mark Zuckerberg, striking back at the activists:

But Facebook’s founder Mark Zuckerberg said it was “not sustainable to offer the whole internet for free”.

Mr Zuckerberg said that people should not prevent others from using the internet in order to defend an “extreme definition of net neutrality”.

“Are we a community that values people and improving people’s lives above all else, or are we a community that puts the intellectual purity of technology above people’s needs?” he asked.

In announcing the Internet.org Platform, Zuckerberg says “For most people who aren’t online, the biggest barrier to connecting isn’t lack of infrastructure – more than 80% of the world’s population already lives within range of a mobile signal. Instead, the biggest challenges are affordability of the internet, and awareness of how internet services are valuable to them.”

Should carriers and applications be restricted in exploring business models that increase adoption of digital technology and services? Or, as Zuckerberg asks, will an “extreme definition of net neutrality” put “the intellectual purity of technology above people’s needs?”

I find it interesting to see how two of Canada’s most important telecom trading partners are approaching net neutrality.

Recall, earlier this year I wrote “Canada’s policy framework for net neutrality is among the most prescriptive and restrictive.” A month later, I asked if Canada should be considering a review of its network neutrality policy.

South of the border, we see the FCC looking at imposing network neutrality regulation through a recategorization of internet services under Title II. And the UK’s regulator, Ofcom, has recently concluded a year long review and it has announced that the UK is heading in the opposite direction, revising its network neutrality guidelines to relax earlier rules. Ofcom’s Director of Connectivity, Selina Chadha, is quoted saying:

The net neutrality rules are designed to constrain the activities of broadband and mobile providers, however, they could also be restricting their ability to develop new services and manage their networks efficiently.

We want to make sure they can also innovate, alongside those developing new content and services, and protect their networks when traffic levels might push networks to their limits. We believe consumers will benefit from all providers across the internet innovating and delivering services that better meet their needs.

In the UK, certain aspects of net neutrality are imposed under Parliamentary legislation. Ofcom is responsible for monitoring and ensuring compliance and cannot change the legislation itself.

ISPs can offer premium quality retail offers: Allowing ISPs to provide premium quality retail packages means they can better meet some consumers’ needs. For example, people who use high quality virtual reality applications may want to buy a premium quality service, while users who mainly stream and browse the internet can buy a cheaper package. Our updated guidance clarifies that ISPs can offer premium packages, for example offering low latency, as long as they are sufficiently clear to customers about what they can expect from the services they buy.

ISPs can develop new ‘specialised services’: New 5G and full fibre networks offer the opportunity for ISPs to innovate and develop their services. Our updated guidance clarifies when they can provide ‘specialised services’ to deliver specific content and applications that need to be optimised, which might include real time communications, virtual reality and driverless vehicles.

ISPs can use traffic management measures to manage their networks: Traffic management can be used by ISPs on their networks, so that a good quality of service is maintained for consumers. Our updated guidance clarifies when and how ISPs can use traffic management, including the different approaches they can take and how they can distinguish between different categories of traffic based on their technical requirements.

Most zero-rating offers will be allowed: Zero-rating is where the data used by certain websites or apps is not counted towards a customer’s overall data allowance. Our updated guidance clarifies that we will generally allow these offers, while setting out the limited circumstances where we might have concerns.

Professor Mark Jamison of the University of Florida’s Public Utility Research Center writes that “net neutrality is a concept whose time has passed.” Instead of relying on rules tailored for the digital age, the FCC is planning to bring internet service providers under Title II. These were regulations originally developed for monopoly wireline telephone services. opens the door for all the old laws to apply.

Professor Jamison notes that the proposed regulations are introducing a ‘general conduct standard’ “that grants the FCC authority to prohibit anything it deems ‘unreasonable.'” He argues that in an era of such rapid technological advancements, regulators need to make decisions (based on sound evidence) and adopting a ‘light-handed regulatory approach.’

Should the CRTC undertake a review similar to that which was done by Ofcom? Like the UK, would Canada find that the current environment may be restricting the ability to develop new services and manage networks efficiently?

Does the CRTC have the resource capacity to take on yet another review as it implements the government’s Online Streaming and Online News Acts?

because the net neutrality rules constrain the activities of the ISPs, they may be seen as restricting their ability to innovate, develop new services and manage their networks. This could lead to poor consumer outcomes, including consumers not benefiting from new services as quickly as they should, or at all. These potential downsides might become more pronounced in the future, as people’s use of online services expands, traffic increases, and more demands are placed on networks.

As Ofcom has noted, as technology evolves and we continue to move even more activities online, it is important for net neutrality regulations “to support innovation, investment and growth, by both content providers and ISPs. Getting this balance right will improve consumers’ experiences online, including through innovative new services and increased choice.”

ISPs have flexibility to offer retail packages with different levels of quality;

ISPs can use traffic management measures to manage networks;

ISPs have more scope to develop specialised services, such as network slicing;

Ofcom will not prioritise enforcement action where there is clear public benefit, in relation to:

the prioritisation and zero-rating of all communications with the emergency services;

traffic management of internet services provided on transport;

the use of parental controls and other content filters involving the blocking of traffic; and

blocking access to fraudulent or scam content.

Last week, I thought it was interesting that the CRTC itself chose a more nuanced approach to zero-rating in its determinations in TRP CRTC 2023-41: Mobile wireless service plans that meet the needs of Canadians with various disabilities. In that policy determination, the question of permitting (and even mandating) zero-rating was at issue for Video Relay Service (VRS). The CRTC found that “zero-rating VRS clearly benefits the public interest, with minimal associated harm, and would be consistent with the DPP (Differential Pricing Practices) framework”. Still, the CRTC did not consider it to be necessary to mandate zero-rating of VRS by all of the service providers, finding that consumers have access to competitive choice of providers that offer zero-rated VRS services and other suitable solutions.

Competitive choice, freedom to innovate and develop new services. Those might be clues that the CRTC should reassess its overly prescriptive approach to net neutrality.

Last week also saw President Biden renominate (for the third time) long-time net neutrality advocate Gigi Sohn to fill a seat on the Federal Communications Commission that has been open for 2 years. David McGarry writes “Should she gain the Senate’s approval, she will break the agency’s current 2–2 Democrat-Republican logjam and allow the agency to re-enact Obama-era net neutrality regulations, which are economically nonsensical and largely unnecessary.”

According to McGarry, “Mandated net neutrality was the worst sort of technocratic overreach. Bureaucrats dreamed up an overbroad market intervention to ameliorate an imagined crisis—to the detriment of innovation and consumers.”

In 2017, Ken Engelhart wrote about the natural experiment created when the the US got rid of its net neutrality regulations under previous FCC Chair Ajit Pai while Canada established its framework.

When Canada banned zero-rating, the United States didn’t. As a result, T-Mobile, an American cellphone company, started zero-rating video services. The other wireless carriers in the U.S. retaliated with unlimited data offers. Now, the U.S. has unlimited wireless offers and Canada doesn’t. Can I say definitively that this is a permanent difference or that it can be attributed to our zero-rating rules? No, but it is the kind of anti-consumer impact that happens when regulators regulate too much.

Two years later, he followed up saying, “You might have expected that as a result two very different internets would develop in the two countries.”

Of course, that didn’t happen. He noted that the US and Canada have similar internet services, with similar average speeds. Indeed, fixed broadband speeds in the US are now about 35% higher than Canada. The sky didn’t fall as predicted by US Senate Democrats.

As Engelhart wrote, “In the end, it seems that public interest groups and regulators were selling the public elephant repellant: a harmless, but useless spray, meant to defend against a threat that does not exist.”

In his 2017 primer on net neutrality, Professor Daniel Lyons wrote, “A small delay in packet delivery may be imperceptible to someone browsing the web but can erode the quality of a video stream or a telemedicine app. Prioritizing these packets could improve the experience for Netflix users or rural doctors, without adversely affecting users of congestion-insensitive services.”

I’ll give Professor Lyons the final word. “More generally, net neutrality discourages innovation by broadband providers. It assumes that the way broadband is currently delivered is the way it must always be, which limits providers’ ability to test new business models.”

Isn’t it time to review Canada’s net neutrality framework?

The UK telecom regulator, Ofcom, has proposed to revise its guidance on how ‘net neutrality’ rules should apply, indicating that a more nuanced approach may be appropriate given the evolution of broadband technologies and the marketplace.

Since the current rules were put in place in 2016, there have been significant developments in the online world – including a surge in demand for capacity, the emergence of several large content providers such as Netflix and Amazon Prime, and evolving technology including the rollout of 5G. So Ofcom has carried out this review to ensure net neutrality continues to serve everyone’s interests.

Ofcom indicated that “the [current] net neutrality rules constrain the activities of the ISPs, [and] may be seen as restricting their ability to innovate, develop new services and manage their networks.” The regulator considered that this could lead to poor consumer outcomes, “including consumers not benefiting from new services as quickly as they should, or at all. These potential downsides might become more pronounced in the future, as people’s use of online services expands, traffic increases, and more demands are placed on networks.”

The consultation document [pdf, 1.5MB] is 139 pages long, plus an additional 62-page set of annexes [pdf, 917KB].

Ofcom is proposing:

most zero-rating offers will be allowed;

ISPs have flexibility to offer retail packages with different levels of quality;

ISPs can use traffic management measures to manage networks;

ISPs have more scope to develop specialised services, such as network slicing;

Ofcom will not prioritise enforcement action where there is clear public benefit, in relation to:

the prioritisation and zero-rating of all communications with the emergency services;

traffic management of internet services provided on transport;

the use of parental controls and other content filters involving the blocking of traffic; and

blocking access to fraudulent or scam content.

Ofcom has also proposed additional reporting from ISPs to allow monitoring the effects of the increased flexibility being provided.

Ofcom is also seeking comment on providing greater flexibility for ISPs in certain areas that could generate positive consumer outcomes, but are not permitted under the current legislation, including: allowing zero-rated content to be accessed after a customer’s data allowance has been exhausted; allowing retail offers which guarantee different quality levels for traffic associated with specific content; and allowing greater flexibility to apply traffic management to specific content to address congestion.

Finally, Ofcom has provided views on “the possibility of allowing ISPs to charge content providers for carrying traffic that might lead to more efficient use of networks.”

We acknowledge that in principle there could be benefits to a charging regime, particularly in improving the incentives on CAPs to deliver traffic efficiently. However, we also recognise the difficulties that designing an effective scheme raises, the risks and uncertainty such a change could create, and the unclear impact on consumers. A charging regime would be a significant step and we have not yet seen sufficient evidence that such an approach would support our objectives at this time. We also consider our other proposals provide flexibility that should help mitigate several issues identified by ISPs.

Comments are due January 13, 2023. Ofcom says that it expects to issue its decision and revised guidance by Autumn 2023.

“We want to make sure that as technology evolves and more of our lives move online, net neutrality continues to support innovation, investment and growth, by both content providers and ISPs. Getting this balance right will improve consumers’ experiences online, including through innovative new services and increased choice.”

As some will recall, prior to becoming a talk show host, Stephen Colbert starred as a right-wing pundit on a satirical news show entitled The Colbert Report. Colbert, the pundit, was billed as America’s most fearless purveyor of “truthiness”. What is truthiness? It’s “the belief or assertion that a particular statement is true based on the intuition or perceptions without regard to evidence, logic, intellectual examination, or facts”.

Giving elected officials the chance to ask questions of regulators is an important part of our democratic process. It can be very informative when used wisely. Unfortunately, the opportunity is wasted if Committee members are unprepared or do not have a solid understanding of the industries they are overseeing.

There was a lot of truthiness on display at INDU as Committee members repeated inaccuracies about wholesale internet access rates, the state of competition in the wireless industry, the reasons for the lack of foreign entry, and the role of MVNOs in the wireless market. Some of these topics were discussed in my post last year (“Mythbusting Canadian Telecom”), but these misunderstandings refuse to go away and deserve revisiting.

Myth #1: The CRTC raised wholesale internet access rates

Few regulatory files have been as misunderstood as the setting of wholesale rates for internet service providers (ISPs) dependent on using facilities of carriers that have invested billions in building Canada’s digital infrastructure. These reseller ISPs operate using connections built by wireline carriers, paying wholesale rates that are set by the CRTC.

For as long as I have been around, these rates have been in dispute. Indeed, the interconnection architectures have been subjects of multiple regulatory battles as independent service providers seek alternate ways to arbitrage the connections provided by the facilities-based service providers [see, for example, the CRTC’s wholesale services framework set in July 2015].

The latest rates dispute actually began in May 2015, when the CRTC began a “Review of costing inputs and application process for wholesale high-speed access services.” In early 2016, the CRTC resolved that consultation and made a determination on processes to set the wholesale rates. In October 2016, the CRTC established substantially lower wholesale rates that it designated as “interim” while it undertook a more extensive review. These interim rates reduced the transport component by up to 89%, and the access component rates by up to 39%. Notably, at the time, CNOC issued a statement saying “The CRTC’s actions will immediately benefit both Canadian consumers and businesses and we are hopeful that the final outcome of this matter will have the same result.”

In 2019, the CRTC issued its “final” determination, setting rates that lowered the rates even more, rates that the Commission later acknowledged were based on mistakes. Those 2019 wholesale rates were never given effect; the 2019 decision was immediately made the subject of multiple channels of appeal and the rates were stayed. In May 2021, the CRTC finalized the rates and issued a wholesale broadband service background paper describing the process.

As the CRTC Chair told INDU, “When we analyzed the evidence, we found errors and could no longer justify the associated rates. Ultimately, we chose to reaffirm and make final the interim rates that we set in 2016, with some adjustments.”

Most importantly, as INDU was told, “the 2019 rates were never in effect in the marketplace.”

The CRTC did not raise wholesale internet access rates. It lowered them.

Myth #2: Canada has a lack of competition compared to other countries

Many have heard it said that the Canadian wireless market is less competitive and more concentrated than in other countries. But how many making such statements have bothered to look at the state of competition in other markets?

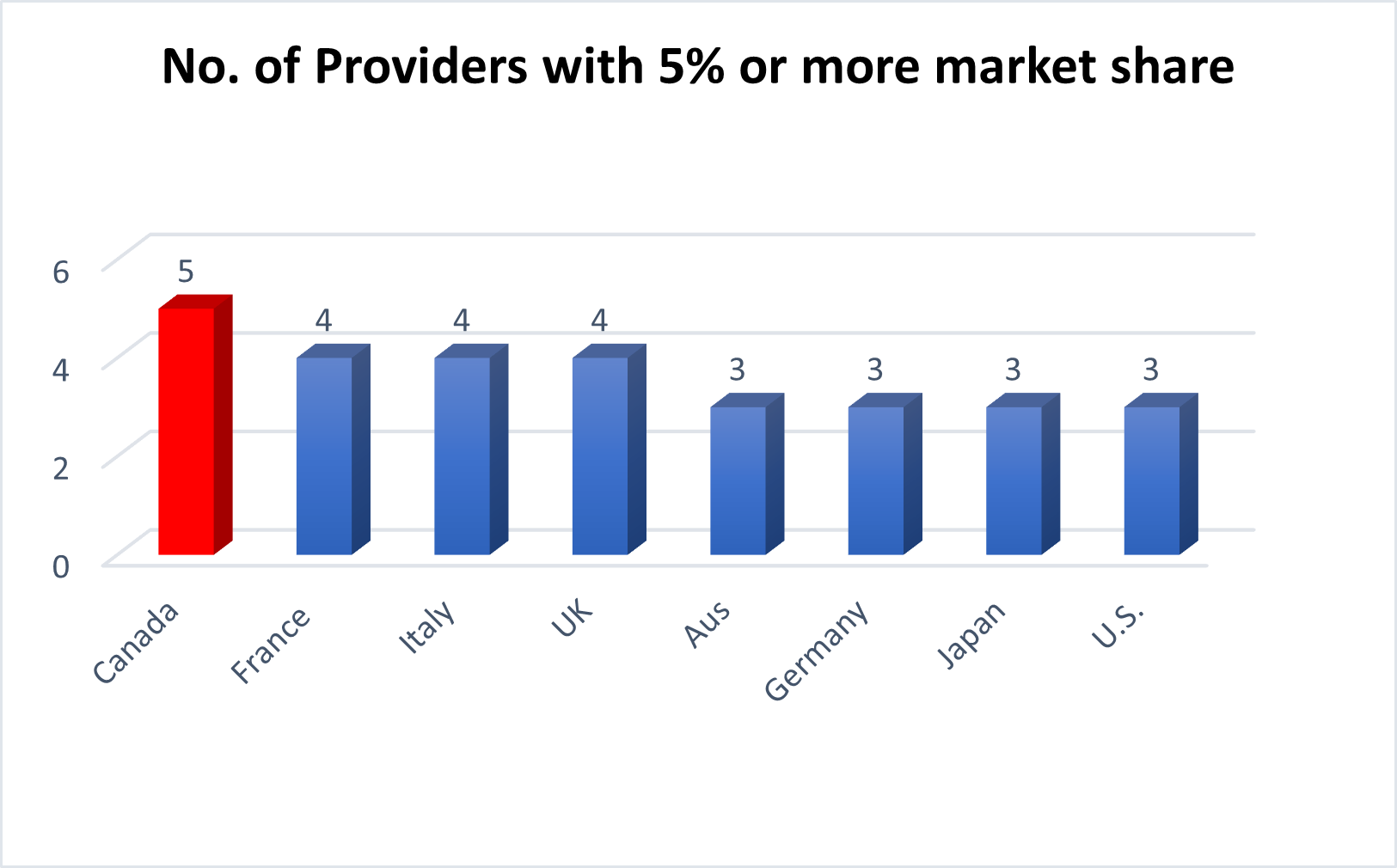

Figure 1

I decided to do just that.

[Note: The data in Figures 1 through 4 is from Telegeography (September 2021). The source data for Figure 5 is The Economist Intelligence Unit – The Inclusive Internet Index – 2021]

One way to look at competition is by the number of mobile wireless carriers in each market. If you listen to some commentators, you might assume that Canada has fewer carriers than most other countries.

In fact, the opposite is true.

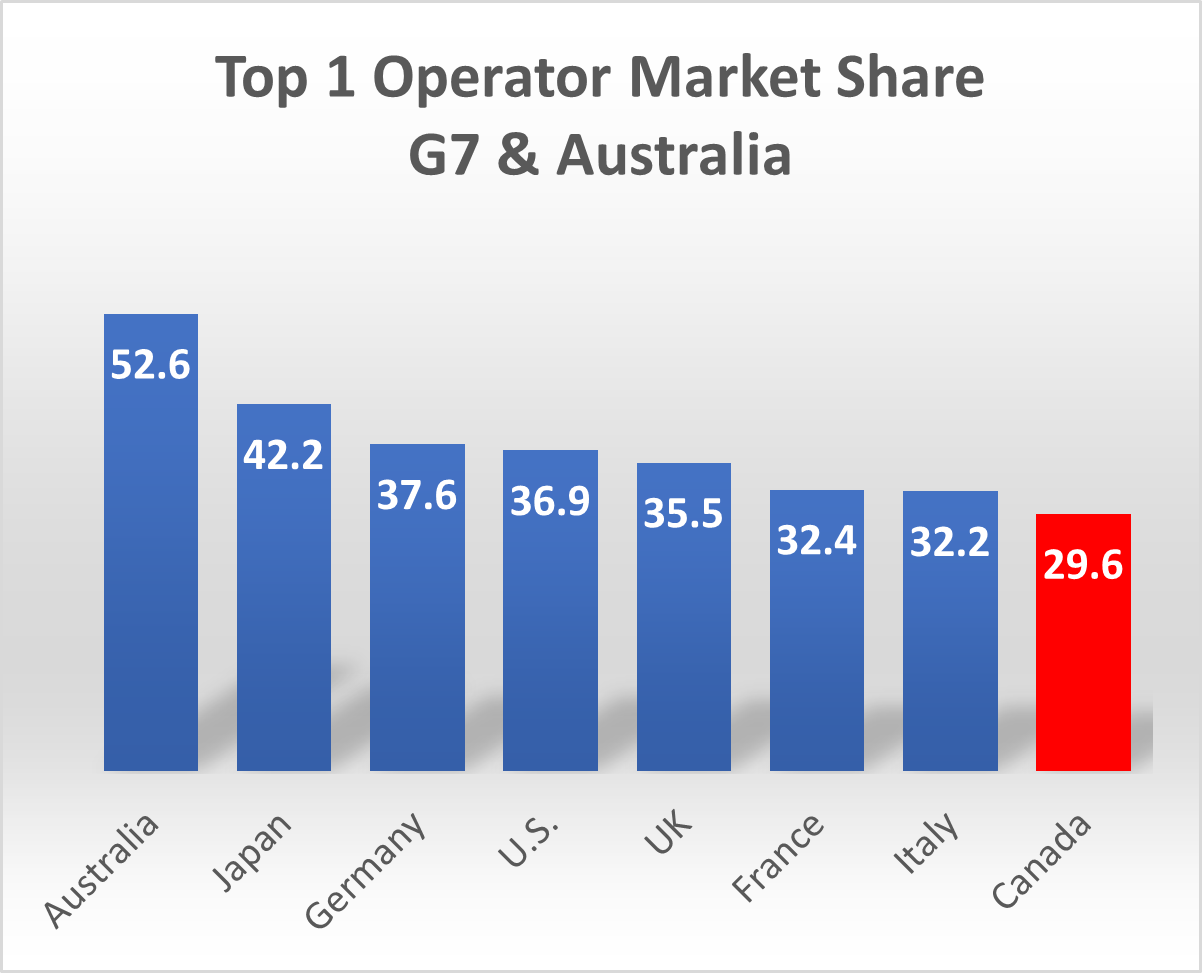

Figure 2

As shown in Figure 1, Canada has more mobile service providers with a 5% market share than any other country in the G7 plus Australia.

Some may respond by saying that despite having five carriers that surpass the 5% threshold, Canada’s three national carriers dominate the market.

Figure 3

Sure, the national carriers are bigger than the regional providers, but does that make Canada an outlier compared to its peers?

The facts show otherwise.

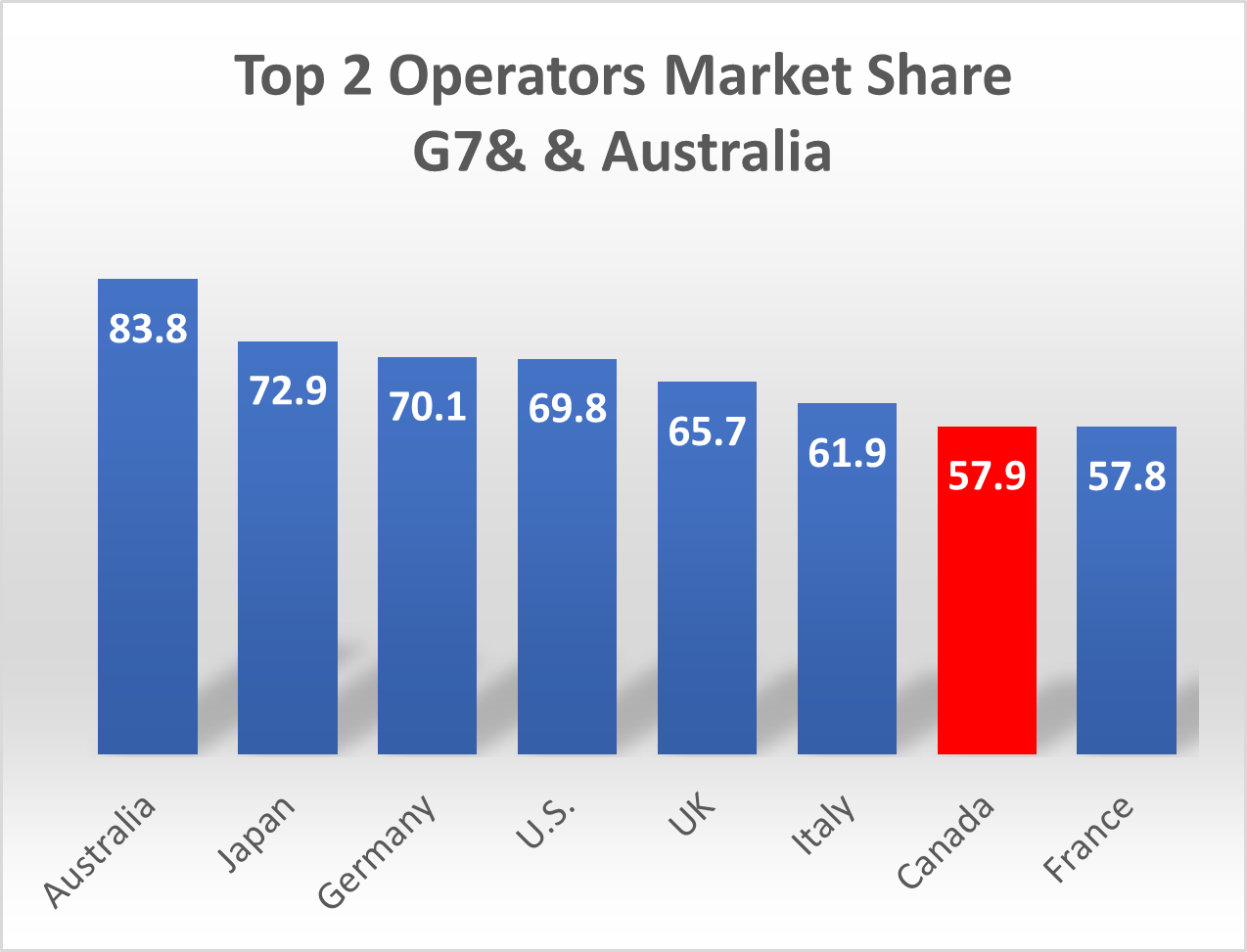

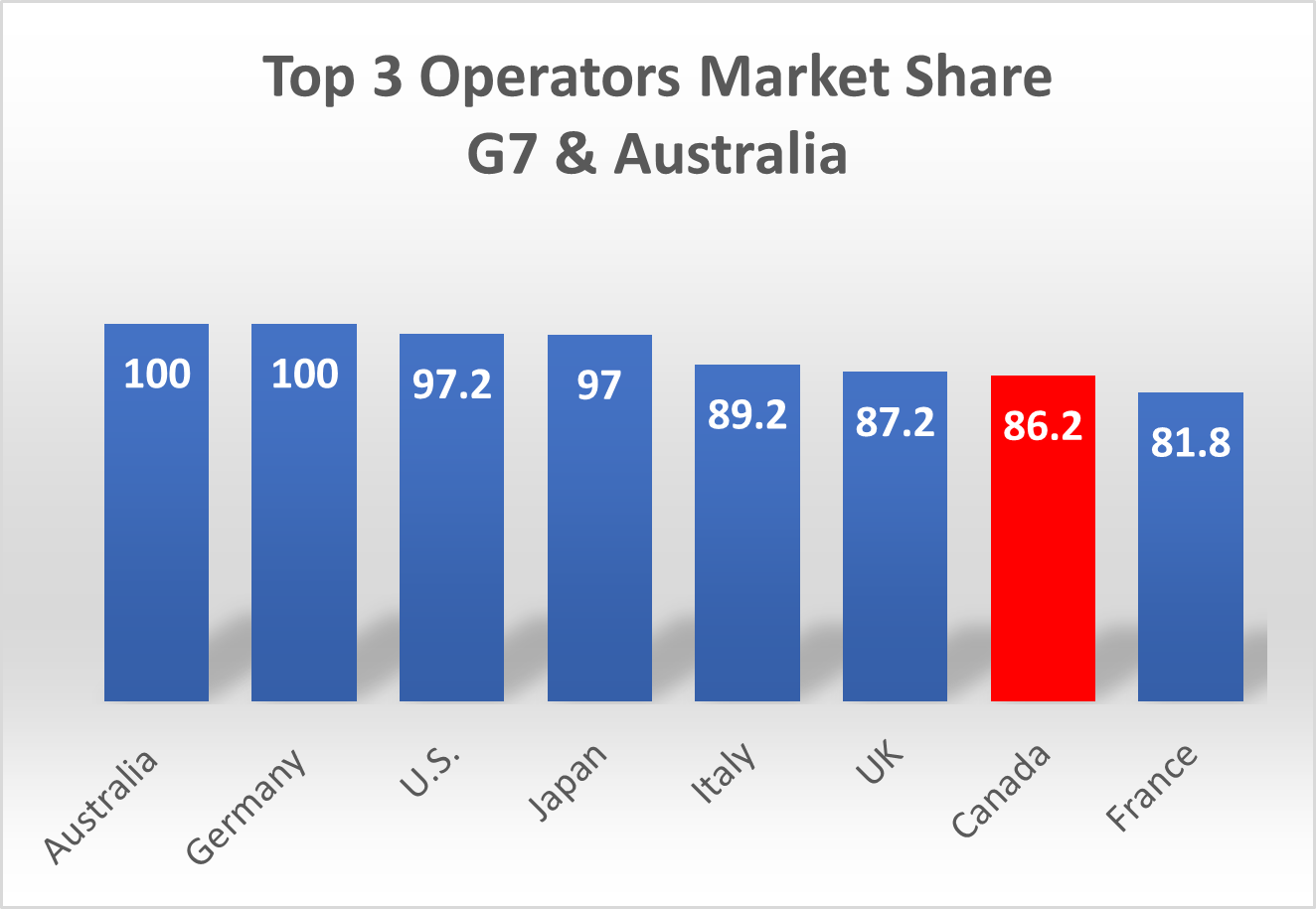

Figures 2, 3 and 4 illustrate that Canada’s wireless market is less concentrated than peer countries (other than France) when you look at the market share of the leading carrier, the share of the top two carriers, and the top three carriers.

Figure 4

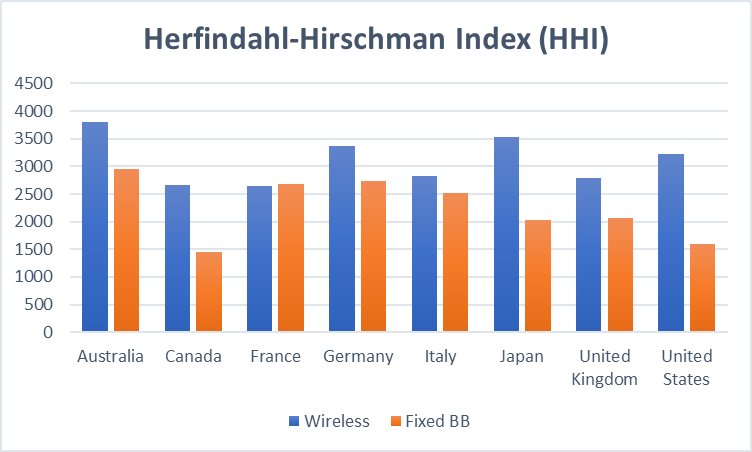

Another commonly accepted measure of market concentration is the Herfindahl-Hirschman Index (HHI). HHI is calculated by squaring the market share of each competing firm and then summing the result.

An HHI of 10,000 would indicate one company in a market with 100% market share, while a market of thousands of firms, each with less than 1% market share would have an HHI of close to zero. In other words, the lower the HHI, the less concentrated a market is.

Figure 5As Figure 5 illustrates, of the G7 countries plus Australia, Canada has the lowest HHI for fixed broadband markets and is in a virtual tie with France for lowest wireless market HHI.

Despite these facts, critics of Canada’s wireless industry continue to argue that a lack of competition is the cause of whatever aspect of the market they are rallying against.

Since it isn’t the competitive intensity, perhaps more attention should be paid to other factors that distinguish Canada from other countries.

For example, readers of this page know that I have frequently discussed the high quality and expansive coverage of Canada’s digital infrastructure, despite substantially higher costs associated with spectrum and building networks to serve Canada’s widely-dispersed and smaller population.

Myth #3: More MVNOs would reduce prices in Canada

At INDU, one MP suggested that the CRTC said “no” to Mobile Virtual Network Operators (MVNOs).

No, the CRTC did no such thing.

The Commission refused to mandate MVNOs, but that is the same as virtually every regulatory body around the world. And similar to most jurisdictions, MVNOs are indeed permitted in Canada.

And MVNOs actually exist in the Canadian market. But, implicit in the MP’s questioning was the idea that having more MVNOs would result in lower consumer prices. It’s an appealing argument, until you look at the facts and understand that the objective of MVNOs is not to lower prices, it is to make a profit.

Outside of China, the countries with the largest MVNO market are the US, Germany, and Japan. It is estimated that Japan has about 170 MNVOs. If there were a relationship between the number of MVNOs and lower prices, one would assume that these three countries would also have the lowest wireless prices. They do not. As shown by ISED’s most recent international price comparison report, wireless prices in these countries are similar to, and in some cases higher than, prices in Canada.

So why do these countries have so many MVNOs?

Mobile carriers in these countries decided that part of their business strategy would be to use resellers and other brands to acquire customers for their network services. In some cases, they use a sub-brand that they own; in other cases, they enter into a commercial arrangement with an independent brand. For the independent brand, the motivation is not to lower prices; like all businesses, their objective is to make a profit. Some were successful by targeting specific demographics or brand-aware groups, while many were unsuccessful and have gone out of business. But the bottom line remains: the number of MVNOs does not correlate to lower prices.

Myth #4: Foreign companies are not allowed to offer wireless services in Canada

I continue to be surprised at the persistence of this myth. But even more surprising was to hear a Conservative MP raise the issue at INDU, when almost ten years ago the Conservative-led government removed nearly all restrictions on foreign companies operating in the Canadian wireless market. The only remaining restriction is a foreign-owned company cannot gain entry by acquiring any of the three national carriers.

What is stopping them from launching a competing wireless business in Canada? I can only speculate, but I think it is reasonable to assume that they have looked at the amount of investment required to acquire spectrum and build out a network, the relatively small population of Canada, and, as discussed in Myth 1 above, the number of carriers already in the market, and concluded the business case simply does not work.

It is economics, not regulations, that drives their decision-making.

Why do I continue to address these myths?

I try to tackle these myths for the same reason I write this blog.

You cannot properly oversee a market that you do not understand. Canada and Canadians will not benefit from policies based upon the “truthiness” of feelings and perceptions.

Balancing the policy objectives of quality, network coverage, and affordability requires a deep understanding of the Canadian telecom market, how it compares to other countries, as well as looking at the positive and negative impacts of policy decisions made in other countries to try to avoid unintended consequences.

We can, and must, do better to ensure that the digital networks that helped maintain economic and social activity during the COVID-19 pandemic can propel Canada into a future of economic and social prosperity.

Canada’s future depends on continued investment in connectivity.